Government Subsidies for the Green Steel Transition

By Industrious Labs and Public Citizen

Executive Summary

The global steel industry is responsible for 11 percent of global greenhouse gas emissions due to its reliance on coal. Companies and countries worldwide are investing private and public funds to clean up the steel industry. LeadIT’s Green Steel Tracker has documented 89 decarbonization announcements in the steel industry as of February 2024.

The climate and health impact potential of these projects varies significantly. Upon closer scrutiny, only 33 projects involve direct reduction with hydrogen or direct electrification technologies that could potentially eliminate fossil fuels from steel production, mostly by replacing fossil fuels with green hydrogen made with renewable energy.

Moreover, a mere 10 of them—all in Europe—are set to become large-scale operations with specific plans for using green hydrogen. New research from Industrious Labs and Public Citizen finds that these projects benefit from a median public subsidy of approximately $385 per tonne of iron, approximately 32 percent of a project’s total costs.

The United States trails Europe in offering federal capital expenditure subsidies for green steel initiatives. While the U.S. Department of Energy (DOE)’s Office of Clean Energy Demonstrations has funding for heavy industry through the Bipartisan Infrastructure Law and Inflation Reduction Act, the maximum subsidy available through its Industrial Demonstration Program is ~$250 per tonne of iron produced. That is 35 percent lower than the average subsidy allocated to European green iron projects.

Subsidies are not the only political or economic tool available to accelerate the transition to fossil-free iron and steelmaking. The demand for low-emissions steel is skyrocketing, with an anticipated 6.7 million tons of demand by 2030, primarily driven by sectors like automotive manufacturing. Major U.S. automakers are already committing to sourcing sustainable steel through federally coordinated efforts such as the First Movers Coalition, presenting significant financial opportunities for the steel industry.

In addition, the U.S. steel sector has been a laggard in embracing green steel, and that must change. Governments need industry cooperation to ensure a swift, just transition to sustainable steelmaking. Some projects are moving forward without subsidies as forward-looking European companies actively invest in green steelmaking technologies because of attractive market conditions such as price premiums, corporate climate commitments and labor contracts. Ultimately, the onus to decarbonize is on steel companies.

Transitioning to sustainable steel production is crucial for curbing climate pollution and addressing pressing public health harms in steel communities while creating jobs for the 21st-century workforce. To protect community health and our climate, the government must advance a suite of political and economic tools to support retrofits and new green steel projects. This analysis focuses on one of those tools: the role of public subsidies for capital expenditures and how additional legislation and funding mechanisms can provide globally competitive incentives.

Introduction

The global steel industry is a major polluter

Steelmaking is the largest source of greenhouse gas emissions from heavy industry globally due to its heavy reliance on burning coal. Today, 70 percent of the steel produced worldwide is made with iron ore in coal-burning blast furnaces. Blast furnaces transform iron ore into iron, the foundational element for steelmaking, through a high-temperature process fueled by coke, a purified form of coal. When the methane emissions from mining for coal for steelmaking are factored into the industry’s emissions, the steel industry accounts for a staggering 11 percent of global climate pollution. This is roughly equivalent to the greenhouse gas emissions of the U.S., the second-largest emitting country.

Coal-based steelmaking harms environmental justice communities

In addition to climate pollution, blast furnaces release toxic pollution, including heavy metals and particulate matter, into nearby communities. All seven of the remaining U.S. integrated steel mills are clustered in the Great Lakes region, and many are one of the top three highest emitters for NOx, SO2, particulate matter (PM2.5), and metal chemicals released by all industrial facilities in their state, excluding power plants. These facilities are also known emitters of various carcinogenic chemicals. According to the U.S. Environmental Protection Agency, these pollutants can cause “adverse health effects, including chronic and acute disorders of the blood, heart, kidneys, reproductive system, and central nervous system.”

Table 1: U.S. integrated steel mill emissions ranking among major polluters in their state.

| Owner | Facility Name | Parameter* | NOx Emissions | SO2 Emissions | PM2.5 Emissions | Metal Chemicals Released |

| Cleveland-Cliffs | Burns Harbor | Ranking against 156 major Indiana industrial facilities | #1 | #1 | #1 | #2 |

| Cleveland-Cliffs | Indiana Harbor | #2 | #2 | #2 | #5 | |

| U.S. Steel | Gary

Works |

#4 | #5 | #3 | #1 | |

| Cleveland-Cliffs | Middletown Works | Ranking against 213 major Ohio industrial facilities | #3 | #3 | #1 | #8 |

| Cleveland-Cliffs | Cleveland Works | #9 | #11 | #2 | #1 | |

| Cleveland-Cliffs | Dearborn Works | Ranking against 163 major Michigan industrial facilities | #14 | #5 | #3 | #5 |

| U.S. Steel | Edgar Thomson | Ranking against 219 major Pennsylvania industrial facilities | #20 | #2 | #13 | Unavailable |

*excluding power plants. A #1 ranking indicates the state’s highest emitter. Drawn from 2020 EPA NEI (Point Sources) and 2021 EPA TRI data.

Low-income communities and communities of color disproportionately bear the impacts of integrated steel mill pollution, with the EPA’s analysis showing that 27 percent of people living within 5 kilometers of a steel mill are Black, more than twice the percentage of Black people in the U.S. population. Research by Industrious Labs reveals that people of color and low-income families disproportionately populate communities on the fenceline of the U.S. integrated steel manufacturing plants.

Typically, people of color and low-income households represent roughly 50 percent of the local population surrounding integrated steel mills (both higher than national averages). In cases like Gary Works and Indiana Harbor, the local population is predominantly people of color or low-income. This underscores the historic and current environmental justice harms at the heart of coal-based steelmaking.

Table 2: Demographic information for U.S. integrated steel plants, 3-mile radius.*

| Owner | State | Facility | People of Color

(% of Population) |

Low Income

(% of Population) |

|---|---|---|---|---|

| U.S. Steel | IN | Gary Works | 96% | 63% |

| Cleveland-Cliffs | IN | Indiana Harbor | 96% | 61% |

| Cleveland-Cliffs | OH | Cleveland Works | 60% | 62% |

| Cleveland-Cliffs | MI | Dearborn Works | 47% | 60% |

| U.S. Steel | PA | Edgar Thomson | 37% | 42% |

| Cleveland-Cliffs | OH | Middletown Works | 21% | 48% |

| Cleveland-Cliffs | IN | Burns Harbor | 25% | 24% |

*Industrious Labs’ analysis of EPA’s EJScreen based on 2022 demographic data.

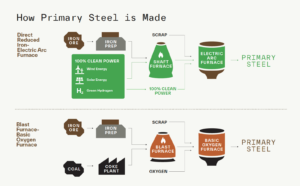

Evolving steel production: from coal to clean technologies

Most steel is made from iron ore using coal in a two-step process:

- Ironmaking: Blast furnaces consume massive amounts of coke and pulverized coal injection (PCI). These materials react with the iron ore to strip it of oxygen and create pure molten iron, or pig iron. This phase in steel production is the principal contributor to the steel sector’s greenhouse gas emissions, also releasing significant pollutants detrimental to human health.

- Steelmaking: Pig iron is then transformed into steel in the basic oxygen furnace.

However, cleaner alternatives to coal-based iron-making are emerging. An alternative two-step process of making iron and steel can potentially eliminate climate pollution:

- Ironmaking: Oxygen is removed from the iron ore at a temperature below the melting point. During this process, hydrogen reacts with oxygen to form water vapor. This method yields various types of direct reduced iron (DRI), including a high-quality product known as hot briquetted iron (HBI). Utilizing green hydrogen, which is generated by electrolyzing water into hydrogen and oxygen with renewable energy, can transform this process into one with near-zero emissions.

- Steelmaking: Pure metallic iron can then be fed into an electric arc furnace (EAF) powered with renewable energy for steel production.

Direct reduced iron (DRI) technology has been used for making iron since the 1970s and is already prevalent in the U.S. market. Currently, three DRI plants in the U.S. in Ohio, Texas, and Louisiana run on methane gas, a climate and health-harming fossil fuel. However, these facilities can be converted to use green hydrogen made from renewable energy, and new DRI plants can be built to run on hydrogen. Mission Possible Partnership estimates that 70 DRI plants will need to be built by 2030 for the steel industry to stay on track with global decarbonization targets.

The U.S. is considered a global leader in EAF technology, with almost 100 facilities nationwide. Most EAFs make steel with recycled scrap and pig iron from blast furnaces. However, they can also use the direct reduced iron or hot briquetted iron produced in a DRI without any modifications. Combining a green hydrogen DRI and a EAF powered by renewable energy can virtually eliminate the fossil fuels used in steelmaking. In this paper, we focus on this technology pathway and abbreviate it to green steel, though other definitions and technology pathways exist.

Other emerging technologies, such as molten oxide electrolysis and other direct electrification approaches, are under development but not yet available commercially at scale globally. As a result, these technologies are not covered in this paper but will likely play an important role in decarbonizing global steelmaking in the future.

U.S. steelmakers can’t afford to miss out on the green steel premium

The U.S. is on the cusp of a steel industry transformation, with an anticipated annual demand of nearly 6.7 million tons of near-zero-emissions steel by 2030. This demand is partly driven by the automotive sector, which is projected to require 3.2 million tons of green steel annually by the decade’s end.

Recent findings from Lead the Charge’s Auto Supply Chain Leaderboard revealed advancements by major U.S. automakers—Tesla, Ford, and General Motors—toward improving the sustainability of their steel supply chains. General Motors and Ford joined the First Movers Coalition, a “global coalition of companies leveraging their purchasing power to decarbonize the world’s heavy-emitting sectors,” including steel. Through this commitment, the companies pledged to source at least 10 percent of their steel from nearly emissions-free providers by 2030. The escalating demand and the potential to secure a 30 percent price premium for clean steel highlights the significant opportunity at the doorstep of the U.S. steel industry.

The green steel transition is a win for workers, public health, and the climate

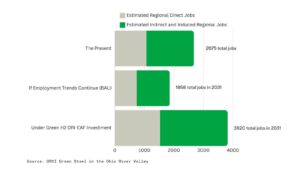

By transitioning to sustainable steel production, the U.S. can slash climate and hazardous air pollution while creating jobs for a 21st-century workforce. A recent report from the Ohio River Valley Institute (ORVI) that assesses transition pathways at the Mon Valley Works integrated steel mill in Pennsylvania found that jobs are expected to decrease by 30 percent this decade under a business-as-usual (BAU) scenario. The threat of job loss is further underscored by examples such as Granite City Works in Illinois, which announced it would indefinitely idle in 2023, putting the future livelihoods of 1,000 workers at risk. Conversely, in the transition to green steel production at the Mon Valley Works, direct and indirect/induced jobs increase by 2031. Investments from state and private actors in steel technologies that rely on renewable energy instead of fossil fuels are both necessary and possible to reshore and repower the domestic steel industry.

Figure 2: Employment projections for the Mon Valley under BAU and green H2-DRI investment trajectories.

Green steel global project landscape

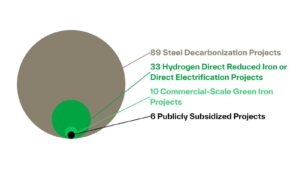

The global push for cleaner steel production is clear, with LeadIT’s Green Steel Tracker documenting 89 announcements for low-carbon investments in the steel industry as of February 29, 2024, spanning from Namibia to Sweden. However, a closer examination of these projects shows that just a fraction of these investments effectively eliminate fossil fuels.

Only 33 projects involve direct reduction with hydrogen or direct electrification processes. Of these projects, only 10 are large-scale plants (0.5 Mtpa, i.e., 0.5 million tonnes per annum) with specific plans for using green hydrogen by 2030. The other 56 projects tracked by LeadIT involve strategies such as the transition of traditional blast furnace-basic oxygen furnace (BF-BOF) configurations to steelmaking-only electric arc furnaces (EAF), the integration of hydrogen blending with methane gas in BF-BOF or DRI, the generation of hydrogen alone (whether green or not), and the implementation of carbon capture and storage (CCS), among others. These investments vary in effectiveness, alignment with green steel standards, and their ability to decarbonize steelmaking.

Figure 3: Breakdown of LeadIT’s tracked steel decarbonization projects.

To assess and accurately compare government subsidies, we focused on the 10 commercial-scale projects expected to produce over 0.5 Mtpa per year, especially the subset of seven projects with clear DRI capacities announced.

Overview of 10 commercial-scale green steel projects

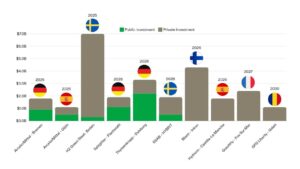

All ten commercial-scale, green hydrogen direct reduced iron (DRI) projects will be built in Europe. Specifically, Sweden and Spain will be home to two projects, Germany with three, while Finland, France, and Romania each have one project planned. Notably, there are no public plans for commercial-scale green hydrogen DRI projects in the U.S.

Figure 4: Total investment (in USD) for green H2-DRI projects by startup year.

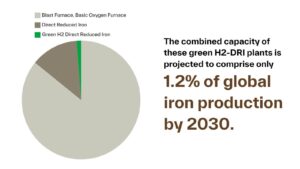

The collective total investment for these projects is $26.6 billion in private and public funds, with six of the projects known to have received public subsidies. The seven projects with specific announced DRI capacities have a collective capacity of approximately 17.6 million tonnes, with additional capacity to come online from the three projects with unknown capacity. The combined capacity of these plants is approximately equal to the U.S.’s current pig iron production of 18.2-22.3 million tonnes over the last five years. However, it’s important to note that the combined output for the project with known capacities will account for just 1.2 percent of global iron production by 2030, based on analysis using projections from Agora and LeadIt’s announcements. This stark figure reinforces the urgent need for global commercial-scale investments in green steel.

Figure 5: Proposed green H2-DRI plants as a percentage of global production.

| Company | Production Plant | Country | Private Investment | Public Investment (Subsidies) | Total Investment | DRI Capacity (million tonnes per annum) | Year Online |

|---|---|---|---|---|---|---|---|

| ArcelorMittal | Bremen** | Germany | $0.9B | $0.9B | $1.8B | Unknown | 2025 |

| ArcelorMittal | Gijón | Spain | $0.6B | $0.5B | $1.1B | 2.3 Mtpa | 2025 |

| H2 Green Steel | H2 Green Steel Boden*** | Sweden | $6.7B | $0.3B | $7.0B | 5.0 Mtpa | 2025 |

| Salzgitter | Flachstahl | Germany | $0.8B | $1.1B | $1.9B | 2.0 Mtpa | 2026 |

| Thyssenkrupp | Duisburg | Germany | $1.1B | $2.2B | $3.2B | 2.5 Mtpa | 2026 |

| SSAB | HYBRIT Gällivare | Sweden | $1.4B | $0.5B | $1.9B | 1.3 Mtpa | 2026 |

| Blastr | Inkoo | Finland | $4.3B | None so far | $4.3B | Unknown | 2026 |

| Hydnum | Castilla-La Mancha | Spain | $1.8B | None so far, but likely | $1.8B | Unknown | 2026 |

| GravitHy | GravitHy (Fos sur Mer) | France | $2.4B | None so far | $2.4B | 2.0 Mtpa | 2027 |

| GFG Liberty | Galati | Romania | $1.1B | None so far | $1.1B | 2.5 Mtpa | 2030 |

| Totals | Subsidized Plants | $11.5B | $5.5B | $17.0B | ~13.1 Mtpa | Known by 2030 | |

| Total | Unsubsidized Plants | $9.6B | None | $9.6B | ~4.5 Mtpa | Known by 2030 | |

| Total | All Plants | $21.1B | $5.5B | $26.6B | ~17.6 Mtpa | Known by 2030 | |

Table 3: Overview of large-scale (>0.5 Mtpa) green H2-DRI projects by start year.*

*All investments converted to USD with assumed exchange rates of 1 SEK = $0.08705 and 1 euro = $1.08225. Gray shading within the table indicates projects without known public subsidies so far. Data drawn from LeadIT’s Green Steel Tracker database and supplemented with recent public announcements.

**This is the estimated investment for the Bremen plant alone. The combined announced private and public investments for Bremen and Eisenhüttenstadt were proportionally allocated based on current ironmaking capacity.

***This number includes investments in upstream hydrogen infrastructure. The subsidy amount does not include financing from the European Investment Bank or loan guarantees.

Public & Private Investments Overview

Public investments in green steel – Europe

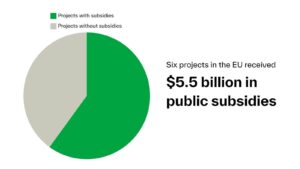

Among the 10 planned commercial-scale, green hydrogen direct reduced iron (DRI) facilities spread across Europe, six have secured public subsidies totaling $5.5 billion. On average, public subsidies cover 32 percent of the total cost of these projects, with combined public and private investments ranging from $1.1 billion to $7.0 billion.

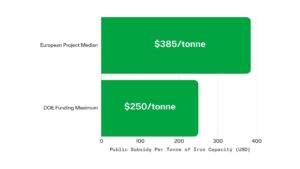

On a per-tonne basis, the median normalized investments for the subsidized plants with known DRI capacity are roughly $385 per tonne in public subsidies and $1,320 per tonne in total investment. Across all plants, including the unsubsidized plants, the median normalized total investment for plants with known DRI capacities is roughly $1,200 per tonne.

It’s important to note that while these projects have secured substantial funding commitments, companies have not yet made a final investment decision (FID). Conflicting statements from major steelmakers, such as ArcelorMittal, have added to the uncertainty. Despite being approved to receive $1.4 billion in subsidies from the German government to construct a DRI and three electric arc furnaces across its plants in Germany, the company recently asserted that hydrogen is too costly to utilize in Europe. This raises concerns, especially considering ArcelorMittal’s contemplation of importing direct reduced iron from other regions to refine into steel in its electric arc furnaces.

Figure 6: Number of proposed green H2-DRI with announced government subsidies.

Public investments in green steel – United States

Contrasting with the European model, potential U.S. federal funding of green steel facilities will likely come through the Department of Energy’s Office of Clean Energy Demonstrations (OCED), created under the 2021 Bipartisan Infrastructure Law to fund advanced clean energy technology projects. OCED has $6.3 billion in funding to accelerate decarbonization across heavy industry sectors via the Industrial Demonstration Program, with project announcements expected in mid-March 2024. However, this federal funding is set to support projects for multiple industrial sectors in addition to steel.

The cost-share model of the Energy Department’s Industrial Demonstration Program—which has a $500 million funding cap per project—has limitations. It stipulates that the U.S. government’s share will not exceed 50 percent of a project’s expenses. Given this framework, a company would likely need to provide a substantial cost share beyond 50 percent to finance a green hydrogen DRI, which data from Europe suggests could cost approximately $2 billion on average. Assuming the average DRI capacity of 2 million tonnes per annum and factoring in the federal cost share limit, the maximum subsidy available from the program equates to ~$250 for every tonne of iron capacity. This amount is 35 percent lower than the median subsidy provided to similar European projects, highlighting the gap in capital expenditure subsidies in the U.S.

Figure 7: Comparison of the median public subsidy per tonne of iron in Europe with the maximum possible subsidy from OCED.

Private investment

It is too early to know if the four European green steel projects without public aid will eventually receive government support or if the business case for green steel will be strong enough to move forward solely with private investment. However, it is promising that these initiatives have each garnered investments of over $1.0 billion in private finance.

Projects that have received public subsidies have also benefited from significant private investment. A prime example is H2 Green Steel securing an additional $4.9 billion for its forthcoming green hydrogen DRI plant in Boden, Sweden. This suggests that U.S. steelmakers can effectively raise private capital to support green steel investments.

Recommendations and Future Outlook for Green Steel in the U.S.

Ten green hydrogen direct reduced iron (DRI) projects in Europe are currently under development, with six receiving considerable government backing. This contrasts starkly with the U.S., where a green hydrogen DRI plant has yet to be announced. This analysis helps contextualize the Industrial Demonstration Program, so American lawmakers can understand what competitive subsidies look like in line with global investments.

While federal support plays a crucial role in easing the transition to greener steelmaking practices, both policymakers and industry stakeholders must recognize the political and economic differences between the U.S. and Europe that allow for different but competitive approaches to government subsidies. While this analysis does not encompass all available subsidies in the U.S. or Europe—notably excluding those impacting the operational costs of green hydrogen—these costs must be considered.

Moreover, the future of green steel cannot rely solely on the availability of subsidies, and steelmakers should not use subsidies as an excuse to delay green steel investments. The cost of inaction is too high. The broader implications for job preservation, community health, and global leadership in technological innovation demand a proactive stance from both the legislative framework and the steel industry itself.

Recommendations for competitive subsidies for capital expenditures:

- Pass new legislation to provide additional funding to the Industrial Demonstration Program or create a new subsidy program that is competitive per tonne of iron capacity to transition existing direct reduced iron plants to green hydrogen.

- Pass new legislation to provide additional funding to the Industrial Demonstration Program or create a new subsidy program that is competitive per tonne of iron capacity to build new, industrial-scale green hydrogen direct reduced iron and other fossil-free technologies.

- Ensure all new federal subsidies for capital expenditures are time-limited and decrease over time to incentivize near-term investments and ensure the U.S. does not miss out on the first mover’s advantage.

The climate crisis demands swift and aggressive action, and decarbonizing the steel sector is an important step. Federal funding must support rapid, ambitious decarbonization measures and prioritize current steelmaking communities as we seek to invest in a homegrown industry supporting working families, community health, and our shared environment. All federal funding must be contingent on robust community benefit agreements consistent with Justice40 principles and the guidelines of Inflation Reduction Act programs, including the Industrial Demonstration Program. These agreements must include representatives of organized labor and the local economic and jobs impact of any proposal, particularly those that seek to transition an existing integrated steel mill away from fossil fuels.

The government can help secure good union jobs, safeguard public health, and protect our climate by deploying a suite of political and economic tools that support retrofits and new green steel projects that implement the most aggressive decarbonization technology possible. Government subsidies for capital expenditures for new green steel plants are one tool that must be considered in the broader political and economic landscape. Effective subsidy programs must put people first and guide industry toward just and equitable investments that build community and worker health and wealth while ensuring that this highly polluting sector transitions to a cleaner future.