Consumers’ Fraught Journey Into Forced Arbitration

A review of the impact that forced arbitration clauses in financial service products have on BIPOC communities

By Candace Milner & Martha Perez-Pedemonti

Introduction and Key Findings

Following the global pandemic of 2019, supply chain interruptions, and high inflation, consumers face many challenges. Individuals, families, and communities have had to keep an anxious eye on the economy while they think about how to make personal ends meet. Anecdotal stories and public data tell us that Americans are being suffocated by debt.[i] Corporations have been engaging in mass layoffs,[ii] workers are striking across industries,[iii] and while unemployment rates remain low, Black and Latinx workers continue to experience higher unemployment rates than white workers.[iv]

As the economic ecosystem continues to ebb and flow, financial institutions have consistently expanded their products and shifted how consumers bank, borrow money, and make purchases. While the impact of these shifts is often vast and unpredictable, something that has remained constant is that Black, Indigenous, and other people of color, “BIPOC,” communities are bearing the brunt of the uncertainties that come with these changes.

The courts are a key avenue for consumers to seek accountability when wronged by financial institutions. However, the widespread inclusion of forced arbitration clauses in traditional and emerging financial products undermines consumers’ ability to access courts to obtain relief for corporate wrongdoing. Instead, forced arbitration clauses, located in the terms of service agreements, require consumers to agree —before a dispute even arises between the financial service provider and the consumer—that any disputes must be addressed through arbitration.

The wealth and income gap between white and BIPOC communities is well documented. In 2023, the net worth of Black and Latinx families in the U.S. was $44,900 and $61,600 respectively, compared to $258,000 for white families.[v] Wealth for Black and Latinx families has grown in recent years mostly thanks to the increased value of housing.[vi] Despite this growth, the wealth gap between BIPOC communities and white communities has not decreased in appreciable amounts.[vii]

While many articles and studies that chronicle racial wealth and income gaps cite Asian American and Pacific Islander communities out-earning white households, the truth is that many AAPI communities are navigating widening wealth and income gaps not neatly captured by generalized data.[viii] When data is disaggregated,[ix] it shows that almost half of specified AAPI groups have a smaller median household income than the U.S. median. Income inequality within the AAPI community has increased more than any other racial demographic over the past four decades.[x]

Wealth and income gaps begin to paint a picture of a larger problem: centuries of settler colonialism and systemic racism driven by capitalism. Centuries of intentional policies have continued to widen wealth and income gaps. U.S. economic policies are founded on the institution of slavery and require a permanent working and poor class.[xi] Alongside discriminatory practices and policies, myths about earnings, work ethic, spending, and overall financial literacy have been used to justify the impacts of faulty policy.

The paradox of economic barriers impacting low-income BIPOC communities establishes cycles of poverty that increase the vulnerability of these communities. This report reviews the impact forced arbitration clauses in financial service products have on consumers, with a focus on the harms to low-income BIPOC communities, already navigating high economic barriers.

In summary, the report finds that:

Financial service products, including credit cards; money transfer services; and buy now, pay later products, take advantage of the intergenerational impact of wealth and income gaps.

- Across the board, low-income BIPOC communities are preyed upon by unscrupulous financial service providers who insert abusive and predatory clauses, including forced arbitration, in their terms of service contracts.[xii]

Forced arbitration schemes have an especially damaging effect on low-income BIPOC communities.

- Low-income BIPOC communities are already reluctant to engage the courts for assistance.[xiii] The problem of access to courts is made worse still by the prevalence of forced arbitration clauses in consumer contracts. Arbitration systems are further out of reach for low-income BIPOC communities because they are procedurally inaccessible and lack the resources to accommodate marginalized communities. Financial service providers take advantage of the inaccessibility of arbitration forums.[xiv]

- Unlike state and federal court systems, forced arbitration provisions harm low-income BIPOC families, already navigating challenging economic circumstances, by forcing them to engage with arbitration firms that do not provide adequate resources to support low-income BIPOC individuals.

Banning forced arbitration in financial services, as the Consumer Financial Protection Bureau (CFPB) has the authority to do, would be the first step toward granting consumers access to equitable and financial relief.

- Low-income BIPOC consumers would have the ability to file a valid legal claim in court.

- Although far from perfect, state and federal courts offer more diverse judges and juries than arbitration firms, access to public assistance programs, and accessibility services.[xv]

How Public Citizen Conducted this Review

Telling the full story of the financial pitfalls faced by marginalized and disenfranchised communities forced into arbitration agreements based on federal data is not a simple or straightforward endeavor. Methodologies for collecting data are actively being updated by the federal government to address serious gaps. For instance, in January 2023, the Office of Management and Budget (OMB) released initial proposals for updating its race and ethnicity statistical standards, with the focus of improving the quality and usefulness of data collection. The initial proposal further points to the need for collecting more granular data to better understand within-group disparities, to facilitate useful data aggregations, among other purposes.[xvi]

Methodology

As federal agencies and commissions work to update their data-collection methodology to include more granular data, this report relied on a combination of sources including utilizing the limited data available on federal websites, financial service provider websites,[xvii] diverse consumer perspectives, law reviews, journals, news reports, and anecdotal evidence. To the extent that specific terms of service agreements (where available) were reviewed, Public Citizen identified the largest servicers of financial products, by market share and popularity, in three separate categories: credit cards; money transfers; and buy now, pay later products. Public Citizen reviewed each contract for the presence of forced arbitration (and related) clauses, the name of the arbitration forum(s) specified, and whether consumers were provided the option to opt out of the arbitration clause.

Consumer Narrative:

“To anybody publicly reading this complaint, if you don’t opt out, they claim that you can’t sue them in court. If you have the [] rewards card, make sure you opt out of this clause, as it’s [] hidden in very small text. This is beyond deceptive and predatory.”

Consumer Complaint Narrative Submitted to the CFPB No. 3892291, Oct 11, 2020[xviii]

I. BIPOC Communities Entering the Forced Arbitration Consumer Journey

Forced arbitration clauses are found in a wide range of consumer contracts, including contracts governing the purchase of tickets, cellular phone accounts, credit card accounts, accessing a website, downloading an app, residence at a nursing home, and car purchases, among others.[xix] These clauses require consumers to resolve any disputes between them and the company that might arise in the future through private arbitration, rather than in a public court. Forced arbitration clauses also typically bar consumers from joining class action lawsuits. For this reason, in recent years, the number of class actions brought by or on behalf of low-income consumers and employees has drastically dropped.[xx]

Forced arbitration clauses almost always specify the arbitration firm. Because arbitration firms rely on a return-business model to make a profit, the arbitrator has an incentive to rule in favor of the corporation to cultivate a happy return-customer relationship.[xxi] Even when ruling in favor of a plaintiff, arbitrators tend to award less money than juries award to successful plaintiffs.[xxii]

Sometimes, a corporation will provide the consumer with a very small window of time to opt out of, or reject, the forced arbitration clause.[xxiii] Arbitration proceedings are also secret.[xxiv] Proceedings and decisions are not made public.

Myriad circumstances influence how consumers experience financial products. When a consumer is grappling with a tight budget or unmet financial needs, they approach the use of their financial products with a mindset informed by, among other factors, the household’s ability to afford necessities, make big purchases, or even have more cash on hand. The products that consumers encounter in their journeys depend on their needs. If a consumer is trying to cover back-to-school expenses, they may research credit cards; buy now, pay later products; or money transfers. While some consumers can choose between different options when accessing financial products, many consumers are limited because of factors like credit scores, who they bank with, language access, documentation availability, or access to the internet.

When a consumer buys a product or signs up for a service, they will often have to sign a contract or agree to terms of use. At this point, the consumer may encounter a forced arbitration clause, whether they are conscious of it or not. Contracts are often filled with legal language that the average consumer does not understand. Oftentimes, these terms strip consumers of rights—such as the right to go to court to resolve disputes.

Throughout this report there are visuals that illustrate the journey consumers experiencing financial hardship navigate when using financial service products and services. These are hypothetical narratives informed by complaints in the CFPB consumer complaint database, processes outlined in terms of service agreements, and anecdotal evidence.

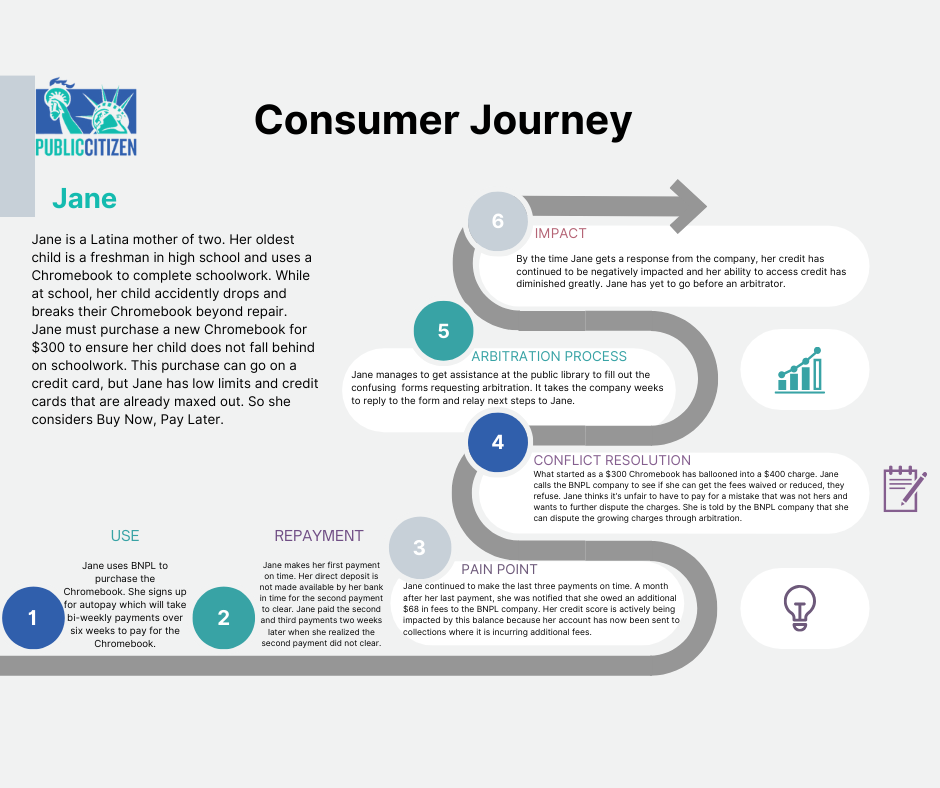

Jane’s Journey

Lack of Diversity in Forced Arbitration

As consumers are funneled into arbitration firms and away from public courts, the pools from which arbitrators are chosen have become a glaring problem because they are neither diverse nor inclusive.[xxv] A 2021 analysis of arbitration firm demographics showed that arbitrators are “mostly men and overwhelmingly white.”[xxvi] The report found that in 2021, 88% of the arbitrators were white and 77% were male at the American Arbitration Association (AAA) and JAMS, the largest arbitration firms in the United States. By comparison, in 2020, women made up 50.9%[xxvii] of the American population, and approximately more than four of every 10 Americans were non-white.[xxviii]

Pursuant to a California law[xxix] requiring consumer arbitration firms to publicize certain data regarding their arbitration practices, AAA and JAMS reported data that allowed us to glean some information about the demographic makeup of arbitrators in California. As to AAA, in 2020, 22% (618 of 2,187) of responding arbitrators[xxx] identified as women. Just 9.3% (just 255 out of 2,256) of responding AAA arbitrators in California identified as American Indian, Alaskan Native, Asian, Black or African American, Hispanic or Latinx, or Pacific Islander, with another 2.7% identifying as another race or more than one race. Regarding gender identity and sexual orientation, just 1.9% (53 of 2,639) of responding arbitrators identified as LGBT+ in California and 4.9% (134 of 2,748) reported having a disability.

The demographics reported by AAA and JAMS[xxxi] do not reflect the demographics of the state of California. One of the most jarring discrepancies observed in this limited data set is the discrepancy between racial diversity in the state of California (65.3%) and the racial diversity in the arbitration pool of AAA (9.3%[xxxii]) and JAMS (16.2%[xxxiii]). Data on gender identity, sexual orientation, and disability status also reveals stark disparities when it comes to arbitrator representation in California.

Arbitrators are people who suffer from prejudices and biases like the rest of the population. A recent academic study analyzing implicit biases in people found that of approximately 61,000, mostly American, participants, despite explicitly affirming the equal humanity of all racial/ethnic groups, white participants consistently associated human-ness (relative to animal) more with white people rather than with Black, Hispanic, and Asian groups in implicit association tests.[xxxiv] Effectively, the study showed that “humanness” was associated with the dominant social group (white) among all participants, especially by white participants.[xxxv]

One of the four threshold criteria to become an arbitrator with AAA is that the applicant possesses neutrality in the form of “freedom from bias and prejudice” and “through an impartial evaluation of testimony and other evidence.”[xxxvi] However, without parameters ensuring that diverse arbitrators are available and hired, consumers will likely continue to be funneled before white male heterosexual arbitrators to decide their claims. At the most basic level, this means that consumer complainants do not get as diverse (in demographics or in numbers) of a panel of decision makers in arbitration as they would in a jury trial.[xxxvii]

Enabled by the random selection of jurors, juries have been described as the most diverse institutions in government.[xxxviii] Evidence suggests that diverse jury pools are more thoughtful in considering racial prejudices, keep individual jurors’ racial prejudices at bay, and are more likely to deliberate for longer periods of time.[xxxix] When coupled with the implicit biases of arbitrators (e.g. unconscious bias against women, BIPOC, LGBTQ+ or persons with disabilities) that impact the worldview of the homogenous arbitrators hearing cases filed by diverse defendants, there is likely to be a negative impact against these populations.

Academic commentators have observed that corporate entities tend not to select women and BIPOC arbitrators, even when more diverse pools are made available.[xl] Intentional racism, implicit bias, stereotypes based on protected classes, and other harmful criteria may also contribute to limiting the number of women and BIPOC arbitrators serving on arbitrator rosters.[xli] If not intentionally using bias in their favor, representatives for corporations may be using principles of risk-aversion to avoid choosing diverse arbitrators because “[d]eviating from the familiar can breed contempt if the result is a loss.”[xlii] In this scenario, if a corporation prevailed using a white-male-heterosexual arbitrator, the corporation will choose a similar arbitrator the next time and the next.

Legal experts argue that a truly random selection of arbitrators, from a diverse pool containing a critical mass of diverse arbitrators, is needed to ensure a more-fair playing field for consumers.[xliii] Underrepresentation of BIPOC and women, especially women of color “[in arbitration pools] calls into question the legitimacy of arbitration as a dispute resolution process regardless of the reason for exclusion of these underrepresented persons.”[xliv] Furthermore, without the inclusion of arbitrators that proportionally represent diverse communities in arbitrator pools, concepts of impartiality, fairness, and neutrality will be undermined by corporate interests that prioritize cost-cutting and winning against the opponent.

The Problematic Process of Arbitration

“While parties do not need an attorney to participate in arbitration, arbitration is a final, legally-binding process that may impact a party’s rights. As such, parties may want to consider consulting an attorney.”

American Arbitration Association, Consumer Arbitration Rules[xlv]

Most consumers don’t have time to review long contracts and don’t have a legal understanding of many contract terms.[xlvi] Moreover, consumers can’t negotiate the terms of consumer contracts for credit cards, cellphones, or other services; to access the service, they have no option other than to accept the terms.[xlvii] Because existing structural barriers tend to keep low-income BIPOC consumers from traditional credit markets, they are at higher risk of exploitation when forced to deal with low-quality, non-mainstream, vendors.[xlviii] One of the most damaging effects forced arbitration clauses have on low-income BIPOC communities, and other marginalized groups, is that they keep lower-income groups from joining in class action, and other forms of aggregate litigation, as a means of bringing small-value and cost-sharing litigation claims before the courts. This means that, without access to the courts, marginalized communities are actively kept from accessing monetary and equitable relief for valid legal claims, becoming aware of existing pitfalls in existing financial products, and ultimately from obtaining monetary relief that may otherwise help them escape the cycle of poverty.[xlix]

Although far from perfect, public courts offer low-income BIPOC litigants access to important resources that assist them in engaging the legal system and pursuing valid legal claims. First, court proceedings are public and subject to scrutiny from legislators, the media, bar associations, and the public. Second, depending on the jurisdiction, civil litigants have access to civil legal assistance programs, court pro se resources, and language access assistance. Finally, although not quantifiable, there is an element of empowerment civil litigants, especially members of marginalized communities, experience when they are able to see and interact with other claimants also seeking to assert their rights and obtain relief for legal claims.

Lack of Consumer Consent

Academic experts agree that empirical research demonstrates that consumers cannot meaningfully consent to arbitration clauses because consumers do not generally comprehend the terms of arbitration clauses.[l] This may be for a number of reasons including the length and complexity of the contract,[li] the manner in which consumer contracts are presented to consumers (as a click-through agreement or in small print),[lii] and the sheer impossibility of reading all of the terms of service that consumers are presented with on a daily basis.[liii] For example, a July 2023 academic study found that over 97% of the study participants reported having opened an account with a company that requires disputes to be submitted to binding arbitration (e.g., Netflix, Hulu, and Cash App), yet most were unaware that they had agreed to arbitration. According to the study, over 99% of respondents who think they have never entered into an arbitration agreement likely have done so.[liv]

The lack of initial contract readership combined with consumers’ inability to access public courts leaves consumers open to exploitation via the use of lengthy contracts filled with legalese.[lv] Deceptive business practices are further likely to target immigrant communities who are more vulnerable due to a confluence of factors including their low bargaining power, limited or bad credit history, limited choices in financial providers, and obstacles to processing information (including language and accessibility barriers).[lvi] This invariably means that consumers often do not read the terms of service contracts until after a problem has arisen.

An academic study suggests that consumers are less likely to seek legal redress for a wrongdoing after realizing they have been harmed due to demoralization that they experience twice before being presented with the opportunity to confront the corporation— first, when the initial wrongdoing takes place and second, after they review that the service contract restricts their legal options.[lvii] The study suggests that consumers may blame themselves for failing to read the terms of service agreement at the time of signing and are therefore less likely to complain or tell others what happened, much less to pursue a claim against the company.[lviii]

Some forced arbitration clauses in consumer contracts provide that the company will pay the arbitration fees. When the consumer must pay, however, filing and fee schedules may be prohibitively expensive, especially for low-income consumers, with filing fees commencing at approximately $225 – $250 with AAA and JAMS, with the potential for consumers to find themselves on the hook for thousands of dollars of expenses, with no right to appeal, if the arbitrator rules against them, depending on the applicable terms of service agreement.

Additional barriers exist for consumers who are indigent or who have accessibility needs. For instance, the AAA Consumer Arbitration Rules state that if a party “wants” an interpreter, they are responsible for making arrangements directly with the interpreter and are also responsible for paying for the costs of the service.[lix] Public Citizen was not able to locate JAMS’ position on language accessibility in its Comprehensive Arbitration Rules & Procedures or its Consumer Arbitration Minimum Standards policy.[lx]

Consumer Narrative

“The Arbitration Provision requires a written, mailed notice to o[p]t-out […] this is inaccessible for blind users.”

Consumer Complaint Narrative Submitted to the CFPB No. 5863990, Aug. 10, 2022.[lxi]

Even when consumers accept a terms-of-service agreement, the agreement can often be changed without their knowledge or consent.[lxii] Corporations can, and often do, update their terms of service agreements at their discretion.[lxiii] Sometimes, corporations update their terms of service in anticipation of, or in the middle of, a legal dispute, allowing them to adopt more favorable terms for themselves.[lxiv]

Consumer Narrative

“I received an email saying that I was now under a binding arbitration agreement, and that in order to opt out of it I have to jump through a series of hoops per their definitions in a timely manner. If they can email me out of the blue changing the terms of a legal agreement, I ought to be able to respond via email. Saying “here’s a binding contract, in order to disagree you have to go buy stamps, take time out of your day, write a letter with 18 pieces of information, etc. … [] is insane.”

Consumer Complaint Narrative Submitted to the CFPB No. 3257389, May 29, 2019.[lxv]

II. The Impact of Financial Service Products on BIPOC Communities

Banks and the financial service industry are well aware of the economic barriers low-income BIPOC communities face. They are also aware that these barriers create gaps for families across the country and a market for products to fill those gaps. Oftentimes we see industry response to these barriers through situations where necessities are purchased on credit; loans are used for larger purchases; and buy now, pay later is used to split purchases so families can still have cash on hand in case of additional emergencies. Access to credit and loans make purchases feasible but they are often a band-aid that is put on a much deeper wound. While there are different theories about the soundness of decisions to use different financial products, consumer behavior shows that when families use these types of predatory services, it is usually a last resort.

Unfortunately, financial institutions market many of their financial products as long-term solutions. In practice, these products are less of a solution and more of a trap. Predatory clauses, enormous fees and penalties, and confusing payback policies tend to become part and parcel of these financial products. The long-term effect is families remain in the cycle of poverty instead of receiving a sound alternative or solution to being cash-strapped in a world where emergencies and unforeseen expenses are certain.

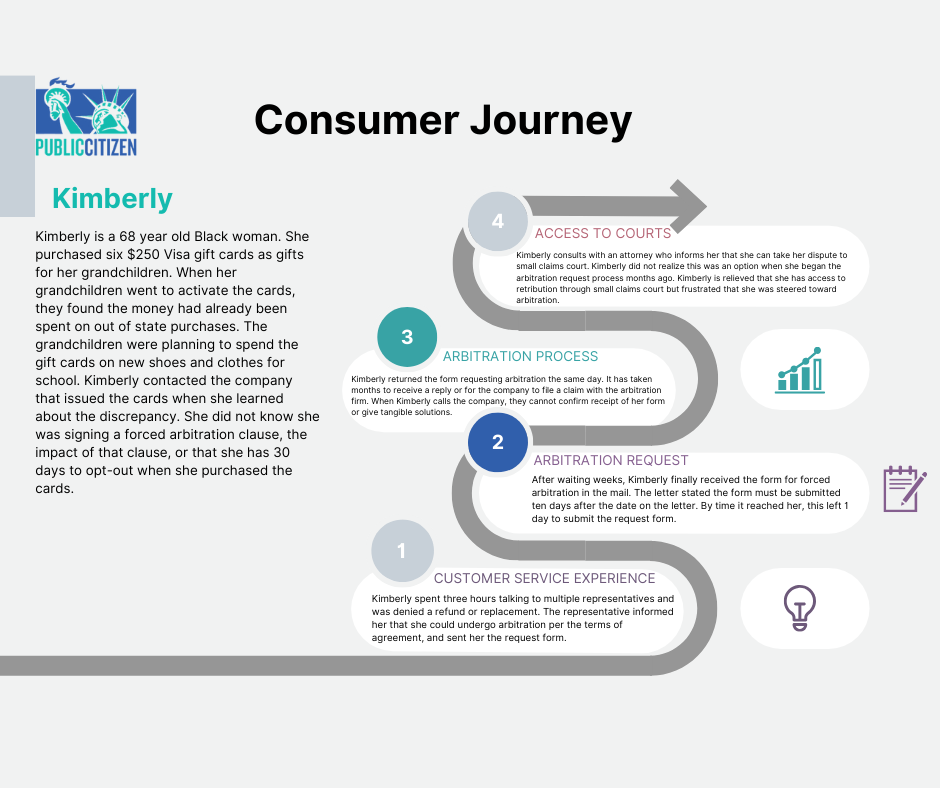

Kimberly’s Journey[lxvi]

Credit Cards and Communities of Color

In 2023, approximately 84% of American adults had a credit card.[lxvii] By racial categories, Black and Latino communities have substantially lower card usage rates than whites with 72% of Black Americans and 77% of Hispanic Americans owning a credit card,[lxviii] as compared to whites at 88%.[lxix] It makes sense that so many Americans use credit cards, they provide people living paycheck-to-paycheck with an essential tool to meet basic needs or cover unexpected bills – a life-vest of sorts.[lxx] Credit cards can be an effective tool to provide immediate access to cash, however debt from credit cards is riskier than some other types of debt due to factors including variable interest rates and late fees, and because credit card debt is generally not tied to long-term assets (like a mortgage, for example).[lxxi]

In 2020 alone, the CFPB found that credit card companies charged $12 billion in late fee penalties.[lxxii] The CFPB reported that subprime cards and private label credit cards (used widely by minorities with sub-prime credit scores) are more susceptible to late fee charges and that consumers residing in low-income areas (with a high concentration of Black residents) bear a disproportionate burden of late fees.[lxxiii] A 2022 study, reported that low-income and Black consumers are more likely to pay credit card fees in comparison to white consumers[lxxiv] and BIPOC consumers are more likely to be offered credit cards at higher interest rates.[lxxv] Against this backdrop, the near universal use of forced arbitration provisions means that when any consumer has a grievance, they are almost certainly going to be forced to arbitrate their claim. Because low-income BIPOC credit card users are more likely to be caught up in problematic terms and conditions, the challenges of being forced into arbitration are especially consequential for these communities.

On average, BIPOC communities make less money than their white counterparts and spend a larger share of their income on necessities such as food, housing, communication, and utilities.[lxxvi] However, recent studies show that credit card rewards (free hotel nights, points for flights) are paid for by low-income credit holders, who are more likely to incur interest charges and late fees that the companies use to offset the cost of rewards.[lxxvii] Moreover, America has some of the highest credit card processing fees (between 2 and 2.5 percent) – fees that impact households with less money more intensely and raise the cost of goods purchased.[lxxviii] For instance, a 2022 study by the Federal Reserve Board estimated a redistribution of credit card rewards totaling $15 billion from poorer, more diverse communities to richer, less diverse, communities.[lxxix]

Consumer Narratives

Following the opening of this account, I did not receive any copy of the Apple Card Customer Agreement, which is required to contain key information about my account such as … important arbitral[tion] terms and conditions… I believe the non-disclosure of such important information has deprived me of my right to be fully informed about the financial product I have purchased … [and] resulted in an unfair and deceptive practice that hampers my ability to make informed decisions regarding my finances.

Consumer Complaint Narrative Submitted to the CFPB No. 7056121, Jun. 1, 2023. [lxxx]

In 2022, Public Citizen reviewed representative samples of the terms of service agreements for the 20 largest credit card issuers in the U.S. by market share and popularity ratings.[lxxxi] In that research, Public Citizen found that 86% of the credit card terms of service reviewed contained forced arbitration clauses. As part of this report, Public Citizen compared the most recent version of the terms of service agreements with those originally reviewed in the 2022 report looking for any significant changes made by companies to credit card agreements in the past year.[lxxxii]

The most prominent changes identified in Public Citizen’s review include, but are not limited to:[lxxxiii]

- Truist Enjoy Beyond Credit Card terms of service agreement expanded the scope of its arbitration clause’s applicability to specifically include disputes concerning the use or disclosure of information. It also added a mandatory pre-arbitration dispute resolution requirement.[lxxxiv]

- Different versions of Citizens Bank Credit Card Agreement F03-AC-6 include different substantive provisions, despite being labeled as the same agreement (F03-AC71-6) and each document stating that it was revised on the same date, April 2022.[lxxxv] The first terms of service agreement was downloaded by Public Citizen in October 2022 (First Agreement); the second terms of service agreement was downloaded by Public Citizen in October 2023 (Second Agreement); and the third terms of service agreement was downloaded by Public Citizen in January 2024 (Third Agreement). As compared to The First Agreement, the Second Agreement deletes boldened language alerting the consumer to the rights they will lose if they do not opt out of the forced arbitration clause[lxxxvi] and inserts language specifying the forum (Rhode Island state or federal court) where any dispute concerning the validity, enforceability, coverage, or scope of the arbitration agreement must be heard. The Third Agreement restores the provisions in the First Agreement.[lxxxvii]

The examples provided above have the potential of having a negative cumulative impact on consumers who are unaware of changes in their credit cards’ terms of service agreements and may have an especially adverse effect on consumers with limited resources.

I called the company that issued the card … and spend[t] 1 hour and 30 minutes on hold. This person took my information and promised to send an “arbitration form” [] and that it would be mailed the next day. I did receive the form … By the time I got the form, I had ONE DAY to send in. Looking on[]line, there are literally THOUSANDS of complaints against this company for fraud, so many that I am astounded they’re still operating.

Consumer Complaint Narrative Submitted to the CFPB No. 5316993, Mar. 3, 2022.[lxxxviii]

In addition to tracking changes to their credit card issuers’ terms of service agreements, the multiple layers of requirements consumers must complete prior to filing an arbitration claim impose procedural, economic, and time-based hurdles that consumers with limited resources and language abilities may be unable to surmount. Table I illustrates the layers of requirements arbitration clauses in terms of service agreements impose on consumers. For instance, some agreements require consumers to engage in mandatory pre-dispute resolution procedures before they can commence formal arbitration proceedings. Forced arbitration clauses also delineate what arbitration service consumers must use, the terms of opt out provisions (if provided), and the procedure for appeal of an arbitrator’s decision (if provided).

Table I: Analysis of Credit Card Terms of Service Agreements[lxxxix] Containing Forced Arbitration Clauses

| Bank and Credit Card | Mandatory Pre-Arbitration Dispute Resolution | Forced Arbitration Clause | Forced Arbitration Firm | Opt-out Provision |

| American Express Gold Card[xc] |

Y | Y | AAA or JAMS | Y |

| Barclays Card[xci] | N | Y | AAA | N |

| Citi Bank Custom Cash Card[xcii] |

N | Y | AAA | Y |

| Citizens Bank Card[xciii] | N | Y | AAA or JAMS | Y |

| Credit One Bank Platinum Visa Card[xciv] | N | Y | AAA | Y |

| Discover Card[xcv] | N | Y | AAA | Y |

| Goldman Sachs GM Card[xcvi] | N | Y | AAA or JAMS | Y |

| HSBC Bank HSBC Master Card Credit Card[xcvii] |

N | Y | AAA | Y |

| JP Morgan Chase Visa Card[xcviii] | N | Y | AAA or JAMS | Y |

| KeyBank National Key2More Rewards Card[xcix] |

N | Y | AAA or JAMS | Y |

| PNC Bank Consumer Card[c] |

N | Y | AAA or JAMS | Y |

| Synchrony Bargain Outlet Card[ci] | N | Y | AAA or JAMS | Y |

| Truist Enjoy Beyond Credit Card[cii] |

Y | Y

|

JAMS | Y |

| US Bank Reserve Card[ciii] |

N | Y | AAA or JAMS | N |

| Wells Fargo Active Cash Card[civ] | N | Y | AAA | N |

Even when consumers attempt to engage in arbitration with their credit card services, consumers are unclear about how to commence arbitration proceedings.[cv] Other anecdotal reports submitted to the CFPB complaint database demonstrate that even when consumers are aware that a forced arbitration clause applies to their dispute, they feel that forced arbitration requirements are inherently unfair.[cvi]

Money Transfer

“If I don’t support her, how will she eat?”

Jesus Perlera, immigrant sending money abroad to support family.[cvii]

In 2021, approximately 14.1% of U.S. households (around 18.7 million households) were underbanked.[cviii] Of that, approximately 4.5% of US households of color (approximately 6 million people) were unbanked, more than 5 times the rate of white households.[cix] Black and Brown Americans represent demographics known to be the most chronically underbanked in America,[cx] making them some of the most vulnerable communities characterized as low-income, lesser-educated, and more likely to come from single-parent homes.[cxi] There is also a cultural aspect to low-income BIPOC communities being unbanked and underbanked related to a general distrust of banks resulting from generations of discrimination against them.[cxii]

Underbanked and unbanked communities are more exposed to cyclical poverty.[cxiii] This is due, in part, because unbanked Americans are forced to pay high fees for everyday financial services like check cashing, money orders, and money transfers.[cxiv] Black Americans have dealt with fluctuating inflation, growing interest rates combined with inequities in affordable and safe housing, wealth accumulation, and educational opportunities that deepened the racial wealth gap.[cxv]

Foreign-born non-citizen Americans are an especially vulnerable population, largely comprised of Asian and Hispanic households. The unauthorized immigrant population in the U.S. was estimated at 10.5 million in 2021, with data demonstrating increases in unauthorized immigrants from nearly every region in the world.[cxvi] Unauthorized migrants primarily travel to the U.S. for safety from war, persecution, violence and human rights abuses, and climate change.[cxvii] The vulnerability of the immigrant community makes them especially exposed to potential exploitation at various points their lived experience – at work,[cxviii] while traveling publicly,[cxix] and as consumers.[cxx]

Approximately 25.7% of all Americans use non-bank money transfer services in the United States, and foreign-born citizens make up 15.5% of that total.[cxxi] The reasons for these transactions are also telling – 25.4% of transactions using non-bank money transfer services are to pay bills, 36.9% are to send or receive money within the United States, and 39.6% were to send or receive international remittances, often to help pay for the cost of living for children and parents living abroad.[cxxii] The cost of sending remittances through money transfer services is fairly high, averaging approximately 5.2% of the total amount being sent.[cxxiii]

A combination of lack of financial resources, lack of time, language barriers, and fear of engaging the court system (let alone arbitration firms’ privatized system) keeps vulnerable communities from seeking legal redress when something goes wrong in their pursuit of sending financial resources to family and friends. Instead, consumers of money transfer services will often accept their loss and find other ways to send money to their loved ones, making them ideal customers for predatory money transfer companies. Armed with the knowledge that the demographics of their customer base is comprised of minority and vulnerable communities, companies take advantage of these factors.

The money transfer companies listed in Table II incorporate various clauses in their online terms of use contracts that obstruct or delay consumers’ ability to file claims in court or through arbitration—with particularly negative consequences for consumers who are unauthorized immigrants with limited resources and/or limited English proficiency. For instance, the majority of the money transfer servicers Public Citizen reviewed operate under at least one other affiliated company, adding to consumer confusion. Additionally, four out of six terms of service agreements reviewed impose forced pre-arbitration requirements, three out of six terms of service agreements fail to provide consumers with the option to opt out of the agreements, and all of the agreements impose forced arbitration on their consumers. See, Table II.

Table II. Forced Arbitration Procedures for Money Transfer Products

| Product | Company | Mandatory Pre-Arbitration Dispute Resolution | Opt-out Provision | Forced Arbitration

Clause |

Arbitration Firm |

| Cash App[cxxiv] | Block, Inc.

(fake Square, Inc.) |

Y | Y | Y | AAA |

| MoneyGram[cxxv] | MoneyGram Payment Systems, Inc. | N | N | Y | AAA |

| PayPal[cxxvi] | Y | Y | Y | AAA | |

| Walmart2Walmart[cxxvii] Powered by Ria | Continental Exchange Services d/b/a Ria Financial Services | Y | N | Y | AAA |

| Wise[cxxviii] | Wise US Inc. | N | N | Y | AAA |

| Western Union, Vigo, Orlandi Valutasm[cxxix] | Western Union Financial Services, Inc. | Y | Y | Y | NAM |

Increasing efforts to protect financial rights of unauthorized immigrants and other vulnerable communities are being made by federal agencies, attorneys general, and state actors.[cxxx] The CFPB has acknowledged that immigrant populations are especially vulnerable to predatory actors because immigrants with no access to mainstream financial services are driven to predatory service providers who “target and mislead immigrant consumers with in-language marketing, convenient access, and familiarity with cultural norms, but without adequate disclosure of terms and conditions.”[cxxxi]

Since 2022, the CFPB has brought enforcement actions against money transfer services engaging in abusive practices on numerous occasions. In April 2022, the CFPB and the New York attorney general announced that they were filing a lawsuit against MoneyGram for systemically and repeatedly violating consumer protection laws by allegedly failing to deliver funds abroad.[cxxxii]

Similarly in October 2023, the CFPB announced that it had taken action against Chime, Inc., another money transfer service, for deceiving consumers about the speed and cost of remittance transfers through its app.[cxxxiii] The CFPB also alleged that Chime illegally forced consumers to waive their legal rights and failed to provide consumers with required disclosures and receipts. The CFPB ordered Chime to refund customers almost $1.5 million in fees and pay a $1.5 million civil penalty into the agency’s victims relief fund.

Buy Now, Pay Later

Buy Now, Pay Later (BNPL) products enable consumers to make a purchase and receive an item while splitting payments over a period of time on a biweekly or monthly schedule.[cxxxiv] Longer repayment schedules often come with higher interest rates. BNPL is like a digital layaway, except the consumer gets the items up front, making BNPL attractive to many consumers because it spreads the financial burden of a purchase. For larger purchases, it enables families to pay little by little and frees up disposable income over the same period. This is especially helpful if you are waiting for future paychecks to pay for a planned purchase that is needed earlier than expected. Additionally, it enables families to buy things on a whim or in an emergency. If your child breaks their laptop and needs a new one for school immediately, BNPL is a tool that can help mitigate the financial drain of purchasing that new laptop even though you did not plan on it.

While BNPL can be a great tool for larger purchases and emergencies, it also has drawbacks. First, continuously using BNPL can stretch a household’s financial obligation if purchases are stacked closely together and thus payments are stacked closely together. BNPL payments are sometimes on an aggressive biweekly schedule which can be overwhelming for a consumer. Next, high interest rates and late fees that take effect if you fail to pay off the purchase in the time allotted can cause debts to balloon and trap consumers in a cycle of debt. Finally, many BNPL debts are reported to collection agencies which can negatively impact consumers’ credit.

Klarna, After Pay, and Affirm are a few of the most popular BNPL platforms available. All three of these platforms have forced arbitration clauses in their terms of service. For each of them, you can opt out of forced arbitration in writing. Klarna[cxxxv] allows consumers to opt out only within 30 days after the first use of the platform. After Pay[cxxxvi] and Affirm[cxxxvii] allow consumers to opt out 30 days after each consumers‘ purchase, for disputes related to that purchase. All three have exceptions for claims filed in small claims court.

Conclusion

Low-income BIPOC communities struggle when funneled into forced arbitration schemes devised to curb consumers’ redress when they are harmed by financial services corporations. Terms of service agreements are individually constructed, and actively revised, to favor corporations, even if it means further marginalizing and destabilizing our most vulnerable communities.

Consumers, especially low-income BIPOC consumers, do not live in a vacuum. They often walk a financial tightrope — balancing the ability to afford day-to-day necessities with the risk of engaging with emerging financial products with more limited resources (time, accessibility) most consumers have.

Intergenerational trauma, racist policies, wealth and income gaps, and general distrust of financial and judicial institutions all play a role when members of low-income BIPOC communities seek relief when wronged by financial service providers. Because having a credit line, driving a dependable vehicle, transferring money to relatives, and purchasing power can all be simultaneous necessities, it is possible for low-income BIPOC consumers to find themselves on multiple forced arbitration journeys at one time. As our consumer journeys demonstrate, struggles paying for day-to-day necessities can intermingle and create a perfect financial storm for vulnerable consumers. Public Citizen’s recommendations for a more equitable system are as follows:

- Pre-dispute forced arbitration clauses in financial products must be banned by the Consumer Financial Protection Bureau. Forced arbitration is unfair to all consumers and especially damaging to our most vulnerable communities.

- The federal government should gather more data quickly. Not enough granular data is available to provide us with a clear picture of how forced arbitration clauses are impacting our most marginalized communities as they engage in day-to-day activities like purchasing products and financial services, transferring money, and accessing credit. Additional data will help lawmakers, states, and federal agencies develop targeted policies that will have far-reaching and impactful effects on these communities.

- Arbitration firms should be required to report on the demographics of their arbitrators, the cases they are hearing, and the outcomes of those cases (equitable and financial relief). This data is crucial to understanding the impact privatized arbitration is having on our communities and how we can hold corporations and arbitration firms accountable for their roles in inequitable outcomes.

- Targeted and accessible public education campaigns for consumers and corporations are necessary and legislation is needed to make this a requirement. Federal agencies and corporations should make materials available in multiple languages and accessible to consumers with disabilities. Financial services corporations should engage their consumers, especially low-income BIPOC consumers, with comprehensive education campaigns not involving fine print traps in terms of service agreements.

[i] Birken, E. G., & Harrison, A. (2023, Nov. 13). Average debt in America: 2023 statistics. USA TODAY. Retrieved Dec. 12, 2023, from https://www.usatoday.com/money/blueprint/debt/average-american-debt-statistics/#:~:text=Americans%20owe%20an%20average%20of,landscape%20in%20terms%20of%20averages.

[ii] Biron, B., Berg, M., Varanasi, L., Hart, J., Delouya, S., McDade, A., & Mayer, G. (2023, Dec. 11), The full list of major US companies slashing staff this year, from Hasbro to Amazon, Business Insider, available at: https://www.businessinsider.com/layoffs-sweeping-the-us-these-are-the-companies-making-cuts-2023.

[iii] Dickler, J. (2023, Oct. 9), Why so many workers are striking in 2023: “Strikes can often be contagious,” says expert, CNBC, available at: https://www.cnbc.com/2023/10/09/from-uaw-to-wga-heres-why-so-many-workers-are-on-strike-this-year.html.

[iv] 2023 Q3 | State Unemployment by Race and Ethnicity. (n.d.). Economic Policy Institute. https://www.epi.org/indicators/state-unemployment-race-ethnicity/.

[v] Luhby, T. (2023, Oct. 31), US Audio Live TV Log In White Americans have far more wealth than Black Americans, Here’s how big the gap is, CNN, Retrieved Dec. 1, 2023, available at: https://www.cnn.com/2023/10/31/us/us-racial-wealth-gap-reaj/index.html.

[vi] Aladangady, A. (2023, Oct. 18), Greater wealth, Greater uncertainty: Changes in racial inequality in the Survey of Consumer Finances, available at: https://www.federalreserve.gov/econres/notes/feds-notes/greater-wealth-greater-uncertainty-changes-in-racial-inequality-in-the-survey-of-consumer-finances-20231018.html#fig1.

[vii] This can be explained partially by consistent racial income gaps. In 2022, the median income for Black and Latinx households was $52,860 and $62,800 compared to $81,060 for white households. See, Income and wealth in the United States: An overview of recent data. (n.d.), pgpf.org, available at: https://www.pgpf.org/blog/2023/11/income-and-wealth-in-the-united-states-an-overview-of-recent-data. When data is disaggregated by gender, the gaps are even larger costing women of color hundreds of thousands of dollars over their lifetime. See, National Women’s Law Center, (2023, Mar. 7), The Wage Gap Robs Women Working Full Time, Year Round of Hundreds of Thousands of Dollars Over a Lifetime – National Women’s Law Center, available at: https://nwlc.org/resource/the-wage-gap-robs-women-working-full-time-year-round-of-hundreds-of-thousands-of-dollars-over-a-lifetime/.

[viii] See, Shih, H. & Khan, R., Hidden in Plain Sight: Asian Poverty in the New York Metro Area, aafederation.org (2021), available at: https://www.aafederation.org/hidden-in-plainsight-asian-poverty-in-the-new-york-metro-area/.

[ix] Clemens, A. (2023, May 1), How data disaggregation matters for Asian Americans and Pacific Islanders, Equitable Growth, available at: https://equitablegrowth.org/how-data-disaggregation-matters-for-asian-americans-and-pacific-islanders/.

[x] As of 2016, the top 10% of the income distribution of AAPI Americans earned 10.7 times more than the bottom 10 percentile. Cultural norms skew this data as AAPI households are more likely to have more working individuals per household than other racial groups. These nuances are important to keep in mind when discussing the economic realities of the AAPI community. Stereotypes extracted from the model minority myth often induce erasure. The stereotypes and framings that suggest AAPI communities are not navigating the same broken economy as the rest of us are harmful tools of white supremacy that must be continuously disrupted as we design solutions to economic barriers. See Kochhar, R. (2020, August 21). Income inequality in the U.S. is rising most rapidly among Asians | Pew Research Center, Pew Research Center’s Social & Demographic Trends Project, available at: https://www.pewresearch.org/social-trends/2018/07/12/income-inequality-in-the-u-s-is-rising-most-rapidly-among-asians/.

[xi] See Desmond, M. (2021, Nov. 9). American capitalism is brutal. you can trace that to the plantation. The New York Times. https://www.nytimes.com/interactive/2019/08/14/magazine/slavery-capitalism.html; Lockhart, P. (2019, Aug. 16). How slavery became the building block of the American economy. Vox. https://www.vox.com/identities/2019/8/16/20806069/slavery-economy-capitalism-violence-cotton-edward-baptist; Openchowski, E. (2022, Aug. 22). New research shows slavery’s central role in U.S. economic growth leading up to the Civil War. Equitable Growth. https://equitablegrowth.org/new-research-shows-slaverys-central-role-in-u-s-economic-growth-leading-up-to-the-civil-war/.

[xii] See, Myriam Giles, Class Warfare: The Disappearance of Low-Income Litigants from The Civil Docket, 65 Emory Law. J. 1531, 1541 (2016).

[xiii] See, Erika Rickard, State Courts Seek to Address Racial Disparities in their Operations, Chief Justices Identify Ways to Implement Reforms as part of Modernization Efforts, pewtrusts.org (Jan. 11, 2021), (“[C]ourt leaders have identified steps that should be taken to reduce racial disparities and acknowledge that people of color, particularly Black Americans, have historically been treated differently by the legal system than their White peers … [s]evere racial disparities are not just an unfortunate byproduct of a race-blind system, but the manifestation of discrimination embedded in the system itself.”).

[xiv] Edmund L. Andrews, Why the Binding Arbitration Game is Rigged Against Customers, gsb.stanford.edu (Mar. 8, 2019), available at: https://www.gsb.stanford.edu/insights/why-binding-arbitration-game-rigged-against-customers.

[xv] See, United States Courts, Comparing Federal & State Courts, Court Structure, uscourts.gov, available at: https://www.uscourts.gov/about-federal-courts/court-role-and-structure/comparing-federal-state-courts. See also, U.S. Department of Justice Civil Rights Division, Federal Coordination and Compliance Section, Language access in State Courts, justice.gov (Sept. 2016), available at: https://www.justice.gov/d9/fieldable-panel-panes/basic-panes/attachments/2020/02/26/language_access_in_state_courts_508_091516.pdf.

[xvi] Federal Register, Notice by the Management and Budget Office, Initial Proposals for Updating OMB’s Race and Ethnicity Standards (Jan. 27, 2023), federalregister.gov, available at: https://www.justice.org/resources/research/forced-arbitration-hurts-women-and-minorities. https://www.federalregister.gov/documents/2023/01/27/2023-01635/initial-proposals-for-updating-ombs-race-and-ethnicity-statistical-standards.

[xvii] Including website terms of service agreement websites.

[xviii] Consumer Financial Protection Bureau, Consumer Complaints, Complaint No. CFPB No. 3892291 (Oct. 11, 2020), consumerfinance.gov.

[xix] As many as 81% of Fortune 100 companies include mandatory arbitration agreements in their mandatory arbitration requirements. See, Larry J. Pittman, Arbitration and Federal Reform: Recalibrating the Separation of Powers Between Congress and the Court, 80 Wash. & Lee L. Rev. 893, 902-03 (2023). See also, Paula Span, Arbitration Has Come to Senior Living. You Don’t Have to Sign Up., nytimes.com (Sept. 24, 2022), available at: https://www.nytimes.com/2022/09/24/health/assisted-living-arbitration.html; Martha Perez-Pedemonti, Report, Regaining the Right to Reject: Forced Arbitration Clauses in Credit Card Contracts, citizen.org (May 15, 2023), available at: https://www.citizen.org/article/regaining-the-right-to-reject-forced-arbitration-clauses-in-credit-card-contracts/; Allison Frankle, Verizon Appeal Will be Early Test of Corporate Strategy to Combat Mass Arbitration, reuters.com (Nov. 22, 2022), available at: https://www.reuters.com/legal/government/verizon-appeal-will-be-early-test-corporate-strategy-combat-mass-arbitration-2022-11-22/; New York Times, The Editorial Board, What Happens When You Click Agree, nytimes.com (Jan. 23, 2021), available at: https://www.nytimes.com/2021/01/23/opinion/sunday/online-terms-of-service.html; Allison Garett, New Update: How the DoorDash and TikTok Cases Will Change the Way Arbitration is Utilized in Class Actions, 2 J. of Dispute Res. 9 (2023).

[xx] See, Myriam Giles, Class Warfare: The Disappearance of Low-Income Litigants from The Civil Docket, 65 Emory Law. J. 1531 (2016). Giles posits that the privatization of the justice system is one of several factors for the observable drop in class actions brought by or on behalf of minority claimants. They further argue that the privatization of the justice system “ha[s] erected a near-impossible obstacles in the path to the courthouse for economically disadvantaged groups.” Id. at 1537.

[xxi] Edmund L. Andrews, Why the Binding Arbitration Game is Rigged Against Customers, gsb.stanford.edu (Mar. 8, 2019), available at: https://www.gsb.stanford.edu/insights/why-binding-arbitration-game-rigged-against-customers. Experts cite a “repeat player bias” existing in these types of arbitrator-corporation relationships where the arbitrator’s bias works more favorably on behalf of the respondent corporations who are repeat players because they have been involved in multiple arbitrations before the same arbitrator. See, Pittman, Arbitration and Federal Reform: Recalibrating the Separation of Powers Between Congress and the Court, 80 Wash. & Lee L. Rev. 893, 901-02 (2023).

[xxii] See, Larry J. Pittman, Arbitration and Federal Reform: Recalibrating the Separation of Powers Between Congress and the Court, 80 Wash. & Lee L. Rev. 893, 902-03 (2023).

[xxiii] Exercising an opt out provision (if one exists) requires a consumer to read through the terms of service agreement to locate the provisions and then follow specific instructions for opting out of the agreement within a narrow window of time (usually 30 to 60 days). See, Martha Perez-Pedemonti, Regaining the Right to Reject: Forced Arbitration Clauses in Credit Card Contracts, citizen.org (May 15, 2023), p. 11, available at: https://www.citizen.org/article/regaining-the-right-to-reject-forced-arbitration-clauses-in-credit-card-contracts/. See also, Barbara Krasnoff, How to Opt Out of Venmo’s New Arbitration Clause, theverge.com (Apr. 25, 2022), available at: https://www.theverge.com/23040916/venmo-arbitration-class-action-sue-how-to.

[xxiv] Moira Donegan, Why Can Companies Still Silence Us With Mandatory Arbitration, theguardian.com (Jan. 8, 2019), available at: https://www.theguardian.com/commentisfree/2019/jan/08/forced-arbitration-sexual-harassment-metoo.

[xxv] See, Megan Lenhard, The huge diversity issue hiding in companies’ forced arbitration agreement, cnbc.com (Jun. 7, 2021), available at: https://www.cnbc.com/2021/06/07/arbitrators-are-male-and-overwhelming-white-heres-why-it-matters.html; and see, Khorri Atkinson, Arbitrator Diversity Lacking as Employers Push to Use Them (1), news.bloomberglaw.com (Mar. 24, 2023), available at: https://news.bloomberglaw.com/daily-labor-report/arbitrator-diversity-still-lacking-as-employers-push-to-use-them.

[xxvi] Research Report, Where White Men Rule: How the Secretive System of Forced Arbitration Hurts Women and Minorities, justice.org (June 2021), available at: https://www.justice.org/resources/research/forced-arbitration-hurts-women-and-minorities.

[xxvii] United States Census Bureau, Census Bureau releases New 2020 Census Data on Age, Sex, Race, Hispanic Origin, Households and Housing, census.gov (accessed on January 17, 2023), available at: https://www.census.gov/newsroom/press-releases/2023/2020-census-demographic-profile-and-dhc.html#:~:text=In%202020%2C%20females%20continued%20to,162.7%20million%20males%20(49.1%25).

[xxviii] Id. See also, Bard Bannon, Opinion: BIPOC lives really do matter in new census report, thehill.com (Aug. 19, 2021) available at: https://thehill.com/opinion/campaign/568537-bipoc-lives-really-do-matter-in-new-census-report/.

[xxix] CA Code. Civ. Pro. § 1281.96 (2022).

[xxx] Arbitration Demographic Data, Demographic Data Provided by AAA Arbitrators and Reported in the Aggregate Pursuant to the California Code of Civil Procedure § 1282.96, available at: https://www.adr.org/sites/default/files/document_repository/ArbitratorDemographicData_01132020.pdf. This is the most recent data AAA has made available as of January 2024. See, American Arbitration Associatoin, Practice Areas, Consumer, AAA Consumer and Arbitration Statistics, available at: https://www.adr.org/consumer#:~:text=Pursuant%20to%20California%20Code%20of,well%20as%20the%20percentage%20of.

[xxxi] JAMS, Panelist Survey 2023, Q1 Demographic Data, JAMS.com, jamsadr.com (accessed on Jan 3, 2023), available at, https://www.jamsadr.com/files/uploads/documents/jams-panelist-demographic-survey-2023.pdf.

[xxxii] This data is based on 2,805 (of 5,562) AAA arbitrators in California, at the time, who responded to the survey. It should be noted that Public Citizen included data points for arbitrators who self-reported as being “some other race” and “more than one race” in this report.

[xxxiii] This data is based on 434 (of 438) JAMS arbitrators in California, at the time, who responded to the survey. It should be noted that Public Citizen included data points for arbitrators who self-reported as being “some other race” and “more than one race” in this report.

[xxxiv] Kristen N. Morehouse, Keith Maddox & Mahzarin R. Banaji, All Human Social groups Are Human, But some are More Human Than Others: A comprehensive investigation of implicit association of “Human” to US racial/ethnic groups, 120 PNAS 22 (2023), available at: https://www.pnas.org/doi/10.1073/pnas.2300995120.

[xxxv] Id. See also, Saul Elbein, Unconscious racial bias goes deep – regardless of views on equality: study, thehill.com (May 23, 2023), available at: https://thehill.com/homenews/4015720-unconscious-racial-bias-goes-deep-regardless-of-views-on-equality-study/.

[xxxvi] American Arbitration Association, Application Process for Admittance to the AAA National Roster of Arbitrators, adr.org, available at: https://www.adr.org/sites/default/files/document_repository/AAA_Application_Process_NationalRoster.pdf.

[xxxvii] See, Larry J. Pittman, Arbitration and Federal Reform: Recalibrating the Separation of Powers Between Congress and the Court, 80 Wash. & Lee L. Rev. 893, 901 (2023).

[xxxviii] Nino C. Morena, Vanguards of Democracy; Juries as Forerunners of Representative Government, 28 UCLA Women’s L.J. 169, 714.

[xxxix] Id. at 179.

[xl] See, Sarah Rudolph Cole, Arbitrator Diversity: Can It Be Achieved?, 98 Wash, U. L. Rev. 965 at 984-985. “Even when provided with candidate lists that include diverse neutrals, businesses seem to default to arbitrators who are either judges or experienced litigators–frequently with backgrounds similar to those who select them. This approach predominantly results in the selection of older, white, male arbitrators because these arbitrators likely have the most experience and name recognition.”

[xli] Id., p. 959.

[xlii] See, Michael Z. Green, Arbitrarily Selecting Black Arbitrators, 88 Fordham L. Rev. 2255, 2273 (2020).

[xliii] See, Michael Z. Green, Arbitrarily Selecting Black Arbitrators, 88 Fordham L. Rev. 2255, 2259 (2020).

[xliv] See, Larry J. Pittman, Arbitration and Federal Reform: Recalibrating the Separation of Powers Between Congress and the Court, 80 Wash. & Lee L. Rev. 893 (2023), 958-59.

[xlv] American Arbitration Association, Consumer Arbitration Rules (Effect. Sept. 1, 2014, Costs Amnd. Nov. 1, 2020), at 21, available at: https://www.adr.org/sites/default/files/Consumer-Rules-Web.pdf.

[xlvi] See, Alex Hern, I Read All The Small Print on the Internet and it Made Me Want To Die, theguardian.com (Jun. 15, 2015), available at: https://www.theguardian.com/technology/2015/jun/15/i-read-all-the-small-print-on-the-internet; and see, David Berreby, Click to Agree With What? No One Reads Terms of Service, Studies Confirm, (Mar. 3, 2017), available at: https://www.theguardian.com/technology/2017/mar/03/terms-of-service-online-contracts-fine-print.

[xlvii] A 2017 Deloitte study found that when faced with no choice, other than to stop using the service, consumers are willing to accept the potential consequences of a user agreement in exchange for access. See, Cakebread infra at n. 51.

[xlviii] See, Myriam Giles, Class Warfare: The Disappearance of Low-Income Litigants from The Civil Docket, 65 Emory Law. J. 1531, 1541 (2016).

[xlix] See, Id. at 1550-1551.

[l] See, Prentiss Cox et. al., Comments of Consumer Law Professors on Petition No. CFPB-2023-0047-0001 (Nov. 14, 2023), available at: file:///C:/Users/mperez/Downloads/CFPB-2023-0047-0014_attachment_1%20(3).pdf.

[li] See, Caroline Cakebread, You’re Not Alone, No One Reads Terms of Service Agreements, businessinsider.com (Nov. 15, 2017, available at: https://www.businessinsider.com/deloitte-study-91-percent-agree-terms-of-service-without-reading-2017-11#:~:text=A%20new%20Deloitte%20survey%20found,consequences%20in%20exchange%20for%20access.

[lii] See, The Editorial Board, What Happens When You Click, nytimes.com, available at: https://www.nytimes.com/2021/01/23/opinion/sunday/online-terms-of-service.html.

[liii] See, David Lazarus, Column: Want to read a tech company’s user agreements? Got 90 minutes to spare?, latimes.com (Aug. 24, 2021), available at: https://www.latimes.com/business/story/2021-08-24/column-consumer-contracts.

[liv] Roseanna Sommers, What do Consumers Understand About Predispute Arbitration Agreements? An Empirical Investigation, papers.ssrn.com (Jul. 25, 2023), available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4521064.

[lv] Myriam Giles, Class Warfare: The Disappearance of Low-Income Litigants from The Civil Docket, 65 Emory Law. J. 1537 (2016).

[lvi] Id. See also, Sonia Lin, Blog: Identifying and Addressing the Financial Needs of Immigrants, consumerfinance.gov (Jun. 27, 2022), https://www.consumerfinance.gov/about-us/blog/identifying-and-addressing-the-financial-needs-of-immigrants/. (Noting that “[w]ith limited or no access to mainstream financial services and products, many immigrants are driven to high-cost or even predatory service providers who charge exorbitant fees or otherwise engage in exploitative practices. Often, these actors target and mislead immigrant consumers with in-language marketing, convenient access, and familiarity with cultural norms, but without adequate disclosure of terms and conditions.”).

[lvii] Meirav Furth Matzkin & Roseanna Sommers, Consumer Psychology and the Problem of Fine-Print Fraud, 72 Stan. L. Rev. 503 (Mar. 2020).

[lviii] Id. From a psychological perspective, Furth-Matzkin and Sommers restate that laypeople (consumers) place excessive weight on written terms (as compared to oral agreements) and therefore feel generally obligated to abide by terms imposed by written contracts, even when the contracts entered into have not been read, the contract is unreasonably lengthy, or the terms are perceived as one-sided or unfair. The authors add “consumers’ lay formalism creates a certain irony: Even though consumers regularly ignore fine print ex ante-before making the transaction–they still regard terms buried in that fine print as binding when they encounter them ex post–when a problem or question arises.” Id. at 516.

[lix] Id. AAA at note 45, R-28 Interpreters p. 22.

[lx] JAMS, Comprehensive Arbitration Rules and Procedures (Eff. June 1, 2021), available at: https://www.jamsadr.com/rules-comprehensive-arbitration/ ; and see, JAMS, Consumer Arbitration Minimum Standards, (Eff. July 15, 2009), available at: https://www.jamsadr.com/consumer-minimum-standards/.

[lxi] Consumer Financial Protection Bureau, Consumer Complaints, Complaint No. CFPB No. 5863990 (Aug. 10, 2022), consumerfinance.gov, available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/5863990.

[lxii] See, Nathan Hutsenpiller, People are Deleting Their McDonald’s App – Here’s Why, parade.com (Oct. 31. 2023), available at: https://parade.com/food/mcdonalds-app-terms-and-conditions.

[lxiii] See, Erik Wemple, Opinion: NYT Exposed the Ills of Forced Arbitration. It’s Now A Company Policy, nytimes.com (Jan 6, 2023), available at: https://www.washingtonpost.com/opinions/2023/01/06/new-york-times-arbitration/.

[lxiv] See, Alison Frankle, Column: Facing Arbitration Onslaught, Samsung Changes Rules for Consumer Claims, reuters.com (Apr. 11, 2023), available at: https://www.reuters.com/legal/transactional/column-facing-arbitration-onslaught-samsung-changes-rules-consumer-claims-2023-04-11/; see also, Jacon Knutson, 23andMe Changes Terms of Service Amid Legal Fallout From Data Breach, Axios.com (Dec. 6, 2023), available at: https://www.axios.com/2023/12/07/23andme-terms-of-service-update-data-breach.

[lxv] Consumer Financial Protection Bureau, Consumer Complaints, Complaint No. CFPB No. 3257389 (May 29, 2019), consumerfinance.gov, available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/3257389.

[lxvi] Partially influenced by CFPB Complaint 5316993, available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/5316993.

[lxvii] Bankrate, Credit Cards, Credit Card Statistics By Race and Ethnicity, bankrate.com (Jun. 7, 2023), available at: https://www.bankrate.com/finance/credit-cards/credit-cards-and-race-statistics/.

[lxviii] Id.

[lxix] Federal Reserve Board Publication, Economic Wellbeing of U.S. Households in 2021, federalreserve.gov (May 2022), https://www.federalreserve.gov/publications/files/2021-report-economic-well-being-us-households-202205.pdf.

[lxx] See, Hannah Pedone & Alexandre Tanzi, Shrinking Minority of Americans Able to Cover $400 Surprise Bill, Bloomberg.com (Aug. 3, 2023), available at: https://www.bloomberg.com/news/articles/2023-08-03/shrinking-minority-of-americans-able-to-cover-400-surprise-bill?embedded-checkout=true. And see, Jessica Dickeler, 62% of Americans are still living paycheck to paycheck, making it ‘the main financial lifestyle,’ report finds, cnbc.com (Oct. 31, 2023), https://www.cnbc.com/2023/10/31/62percent-of-americans-still-live-paycheck-to-paycheck-amid-inflation.html.

[lxxi] See, Christian Weller, Households of Color Owe Costlier, Riskier Debt, Hurting Their Chances to Build Wealth, forbes.com (Dec. 28, 2021), available at: https://www.forbes.com/sites/christianweller/2021/12/28/households-of-color-owe-costlier-riskier-debt-hurting-their-chances-to-build-wealth/?sh=6266fe295600.

[lxxii] Consumer Financial Protection Bureau, CFPB Finds Credit Card Companies Charged $12 Billion in Late Fee Penalties in 2020, consumerfinance.gov (Mar. 29, 2022), available at: https://www.consumerfinance.gov/about-us/newsroom/cfpb-finds-credit-card-companies-charged-12-billion-in-late-fee-penalties-in-2020/.

[lxxiii] The CFPB defines sub-prime borrowers as having a credit score between 580 – 619 and deep sub-prime borrowers as having a credit score below 580. See, Consumer Financial Protection Bureau, Borrow Risk Profiles, consumerfinance.gov, available at: https://www.consumerfinance.gov/data-research/consumer-credit-trends/student-loans/borrower-risk profiles/#:~:text=Deep%20subprime%20(credit%20scores%20below,scores%20of%20720%20or%20above). See also, Id.

[lxxiv] See, Oz Shy & Johanna Stavins, Who Is Paying All These Fees? An Empirical Analysis of Bank Account and Credit Card Fees, Federal Reserve Bank of Boston, bostonfed.org (2022), available at: https://www.bostonfed.org/publications/research-department-working-paper/2022/who-is-paying-all-these-fees-an-empirical-analysis-of-bank-account-and-credit-card-fees.aspx.

[lxxv] See, Jump To, Credit Cards: Pandemic Assistance Likely Helped reduce Balances, and Credit Terms Varied Among Demographic Groups, U.S. Government Accountability Office, gao.gov (Sept. 29, 2023), pp. 25-31, available at: https://www.gao.gov/products/gao-23-105269.

[lxxvi] See, Bureau of Labor Statistics, Table 2200. Hispanic or Latino Origin reference Person: Annual Expenditure Means, Shares, Standard, Errors, and Coefficients of Variation, Consumer Expenditure Surveys, bls.gov (2021), available at: https://www.bls.gov/cex/tables/calendar-year/mean-item-share-average-standard-error/reference-person-latino-2021.pdf.

[lxxvii] Chenzi Xu & Jefferey Reppucci, The Dirty Little Secret of Credit Card Rewards Programs, nytimes.com (Mar. 4, 2023), available at: https://www.nytimes.com/2023/03/04/opinion/credit-card-rewards-points-poor-interchange-fees.html.

[lxxviii] Id.

[lxxix] See, Agarwal, Sumit, Andrea Presbitero, Andr´e F. Silva, and Carlo Wix (2023). “Who Pays for Your Rewards? Redistribution in the Credit Card Market,” Finance and Economics Discussion Series 2023-007. Washington: Board of Governors of the Federal Reserve System, available at: https://doi.org/10.17016/FEDS.2023.007.

[lxxx] Consumer Financial Protection Bureau, Consumer Complaint Narrative No. 7056121, consumerfinance.gov (Jun. 1, 2023), available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/7056121.

[lxxxi] See, Regaining the Right to Reject: Forced Arbitration Clauses in Credit Card Contracts, citizen.org (May 15, 2023), available at: https://www.citizen.org/article/regaining-the-right-to-reject-forced-arbitration-clauses-in-credit-card-contracts/.

[lxxxii] December 2022 to October – December 2023.

[lxxxiii] The examples provided below are only representative examples and do not represent an exhaustive list of the changes observed between the different versions of terms of service agreements compared by Public Citizen for each credit card issuer.

[lxxxiv] See, Truist Bank, Truist Enjoy Beyond Credit Card (Jul. 21, 2023), truist.com, available at: https://www.truist.com/content/dam/truist-bank/us/en/documents/agreement/enjoy-beyond-consumer-credit-card-agreement.pdf. Compare with, Consumer Financial Protection Board, Credit Card Agreement Database, Download all most recent credit card agreements (Q1-2022), Truist Bank, Truist Enjoy Beyond Credit Card Agreement, available at, https://www.consumerfinance.gov/credit-cards/agreements/.

[lxxxv] The first Citizens Bank Credit Card terms of service agreement, labeled F03-AC71-6, was obtained by Public Citizen in or about October 2022; the second Citizens Bank Credit Card terms of service agreement, labeled F03-AC71-6, was obtained by Public Citizen in or about October 2023, and the third Citizens Bank Credit Card terms of service agreement, labeled F03-AC71-6, was obtained by Public Citizen on or about January 2024.

[lxxxvi] Compare, CB Agreement 1 p. 11-12 with CB Agreement 2 p. 11-12.

[lxxxvii] Compare, CB Agreement 1 p. 11-13 to with Agreement 3 p. 11-13.

[lxxxviii] Consumer Financial Protection Bureau, Consumer Complaint Narrative No. 5316993, consumerfinance.gov (Mar. 3, 2023), available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/5316993.

[lxxxix] Specific credit card product reviewed for each issuer is identified in footnote citations.

[xc] See, American Express, American Express Gold Card Cardmember Agreement (Sept. 30, 2023), americanexpress.com, available at: https://www.americanexpress.com/content/dam/amex/en-us/company/legal/cardmember-agreements/public-site-2023-q3-pdf-cmas/cps-charge/american-express-gold-card-09-30-2023.pdf.

[xci] See, Barclays Delaware Bank, Barclays Cardmember Agreement (Jun. 30, 2023), barclaycardus.com, available at: https://files.consumerfinance.gov/a/assets/credit-card-agreements/pdf/barclays-bank-delaware_Standard%20Credit%20Agreement.pdf.

[xcii] See, Citibank, Citibank Custom Cash Card Agreement Guide (2023), citi.com, available at: https://www.citi.com/CRD/PDF/CMA/cardAgreement/CMA_PID416.pdf.

[xciii] See, Citizens Bank, Credit Card Agreement F03-AC71-6, citizensbank.com, available at: https://www.citizensbank.com/assets/CB_PDF/creditcards/CashBackPlusCardholderAgreementSeptember_2023_V1.pdf.

[xciv] See, Credit One Bank, Cardholder Agreements, Card Agreement D233, (Mar. 3, 2023), creditonebank.com, available at: https://www.creditonebank.com/content/dam/creditonebank/corporate-transactional/pdf/cardholderagreements.pdf.

[xcv] See, Discover, Discover Cardmember Agreement (June 30, 2023), discover.com, available at: https://www.discover.com/content/dam/discover/en_us/credit-cards/card-portfolio/cma/pdf/Q4_Pricing_01_Prime_091223.pdf. There are three existing agreements available depending on consumer creditworthiness. Per Public Citizen’s review, all three agreements contain the same arbitration clause.

[xcvi] See, Goldman Sachs, GM Card Terms and Conditions (Jul. 31, 2023), marcus.com, available at: https://www.marcus.com/content/dam/marcus/us/en/pdfs/gm-card-customer-agreement.pdf. In October 2023, it was reported the Goldman Sachs is planning to terminate its co-branded credit cards with General Motors. See, Reuters, Goldman Sachs Plans to Scrap GM Credit Card – Source, reuters.com (Nov. 8, 2023), available at: https://www.reuters.com/business/finance/goldman-sachs-plans-offload-gm-credit-card-source-2023-11-07/.

[xcvii] See, HSBC, HSBC Mastercard Credit Card Cardmember Agreement (Feb. 2023), us.hsbc.com, available at: https://www.us.hsbc.com/content/dam/hsbc/us/docs/pdf/credit-card-pdfs/hsbc-elite-world-elite-cardmember-agreement.pdf.

[xcviii] See, JP Morgan Chase & Co., Chase Cards Visa Agreement (2022), available at: https://www.chase.com/content/feed/public/creditcards/cma/Chase/COL00095.pdf.

[xcix] See, KeyBank, Personal, Credit Cards, Key2More Rewards Mastercard Terms & Conditions, key.com (Jan. 24, 2023), available at: https://www.key.com/personal/credit-cards/key2more-terms-conditions.html.

[c] See, PNC Bank, PNC Bank Consumer Credit Card Agreement # K-10554, pnc.com, available at: https://www.pnc.com/content/dam/pnc-com/pdf/personal/CreditCards/Agreement-Standard-Credit-Card.pdf.

[ci] See, Synchrony Bank, Synchrony Plus World Mastercard Account Agreement (June 2023), synchronybankterms.com, available at: https://www.synchronybankterms.com/gecrbterms/pdf/Synchrony_Plus_World_Mastercard_Account_Agreement_and_Pricing_Addendum.pdf.

[cii] See, Truist Bank, Truist Enjoy Beyond Credit Card (Oct., 2023), truist.com, available at: https://www.truist.com/content/dam/truist-bank/us/en/documents/agreement/enjoy-beyond-consumer-credit-card-agreement.pdf.

[ciii] See, U.S. Bank, Cardmember Agreement for U.S. Bank National Association Visa and Mastercard Classic, Gold and Platinum Accounts (Jun. 30, 2023), usbank.com, available at: https://applications.usbank.com/oad/teamsite/decisioning/usbank/docs/global_default/FR006213482_03_USB.pdf.

[civ] See, Wells Fargo, Wells Fargo Active Cash Credit Card Account Agreement (Aug. 22, 2023), wellsfargo.com, available at: https://www.wellsfargo.com/credit-cards/agreements/active-cash-agreement/.

[cv] See, Consumer Complaint Narrative Submitted to the CFPB No. 6021721 (Sept. 26, 2022) available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/6021721. (“I requested that it be sent to pre-arbitration and Capital One refused to let me.”); Consumer Complaint Narrative Submitted to the CFPB No. 7259402 (Jul. 16, 2023), available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/7259402. (“I requested Capital One to escalate my case to arbitration, and they refused. I provided all documents requested. I spent hours of my time gathering emails and documentation, only to be told Capital One wants additional …”); and see, Consumer Complaint Narrative Submitted to the CFPB No. 6324555 (Dec. 15, 2022), available at https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/6324555. (“I have asked Chase more than 10 times for arbitration as the contract says I have to arbitrate it.”).

[cvi] See, Consumer Complaint Narrative Submitted to the CFPB No. 6663994 (Mar. 9, 2023), available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/6663994. (“Capital One forces [A]merican citizens to agree to terms of service, which strips away our constitutional rights an [A]merican citizen has, considering justice in court is now justice with arbitration paid by the corporation to get one sided results, their own justice. In other words, they are above the law?”). See also, Consumer Complaint Narrative Submitted to the CFPB No. 7335724 (Aug. 1, 2023), available at: https://www.consumerfinance.gov/data-research/consumer-complaints/search/detail/7335724. (“The arbitrator has a track record of siding with merchants approximately 99 % -100 % of the time; otherwise, he would be replaced with an arbitrator who always sided with the corporation supplier. To maintain this arbitration stream of income, the bogus arbitrator simply sides with the corporation against the consumer regardless of the facts.”).

[cvii] Miriam Jordan, Even When They Lost Their Jobs, Immigrants Sent Money Home, nytimes.com (Sept. 24, 2020), available at: https://www.nytimes.com/2020/09/24/us/coronavirus-immigrants-remittances.html.

[cviii] FDIC, 2021 FDIC National Survey of Unbanked and underbanked Households, fdic.gov (Jul. 24, 2023), available at: https://www.fdic.gov/analysis/household-survey/index.html.

[cix] Diane Lincoln Estes, Millions of ‘unbanked’ Americans Lack Adequate Access to Financial Services, pbs.org (Dec. 23, 2022), available at: https://www.pbs.org/newshour/show/millions-of-unbanked-americans-lack-adequate-access-to-financial-services.

[cx] Term used to refer to all Americans living in the United States, regardless of citizenship or legal status.