Public Citizen Testimony Against SB 495 — ESG in Insurance (House Committee Testimony)

Public Citizen Testimony Against SB 495 -- ESG in Insurance (House Committee Testimony)

To: Chairman Jay Dean and the Members of the House Committee on Insurance

CC: Rep. Hubert Vo, Rep. Jessica González, Rep. Vikki Goodwin, Rep. Andy Hopper, Rep. Matt Morgan, Rep. Dennis Paul, Rep. David Spiller, Rep. Trey Wharton

Via hand delivery and by email.

From: Adrian Shelley, Public Citizen, ashelley@citizen.org, 512-477-1155

Re: SB 495, ESG in Insurance – Public Citizen testimony against.

Dear Chairman Dean and Members of the Committee:

Public Citizen appreciates the opportunity to testify against SB 495, relating to the authority of the Texas Department of Insurance to adopt rules that implement or are based on certain environmental, social, and governance models, ratings, or standards. We must oppose this bill because Texas faces significant risk due to weather disasters, insurers are already increasing rates or leaving the state, and rules related to ESG criteria may be necessary to ensure that policyholders are treated fairly.

The bill prevents the commissioner of the Department of Insurance from adopting any rules implementing environmental, social, or governance (ESG) assessments. The bill also forbids a requirement of compliance with any such rule from the National Association of Insurance Commissioners (NAIC). The NAIC has adopted a statement on ESG policies that states, in part:1

The NAIC does not anticipate developing regulatory policy to require or prohibit insurance companies from adopting ESG policies that govern insurers’ underwriting, investing, or other business decisions. However, we have extensive work underway on climate risk, race and insurance, corporate governance, and other related factors to the extent they directly pertain to our responsibility to protect policyholders and supervise the financial health of insurers.

So while the NAIC does not anticipate requiring ESG considerations, it does believe that certain ESG criteria may directly pertain to the protection of policyholders and to the financial health of insurers. How might this play out in Texas?

Texas is the most disaster-prone state.

Since 1980 there have been 403 billion dollar weather disasters in the United States (adjusting for inflation).2 Fully 190 of those disaster have impacted Texas.

That means that 47 per cent of all billion dollar disasters in the United States since 1980 have impacted Texas.

Insurers are already leaving states that are disaster prone. According to Texas Department of Insurance Commissioner Cassie Brown, four insurers left Texas in 2024, with Progressive Insurance becoming the fifth.3

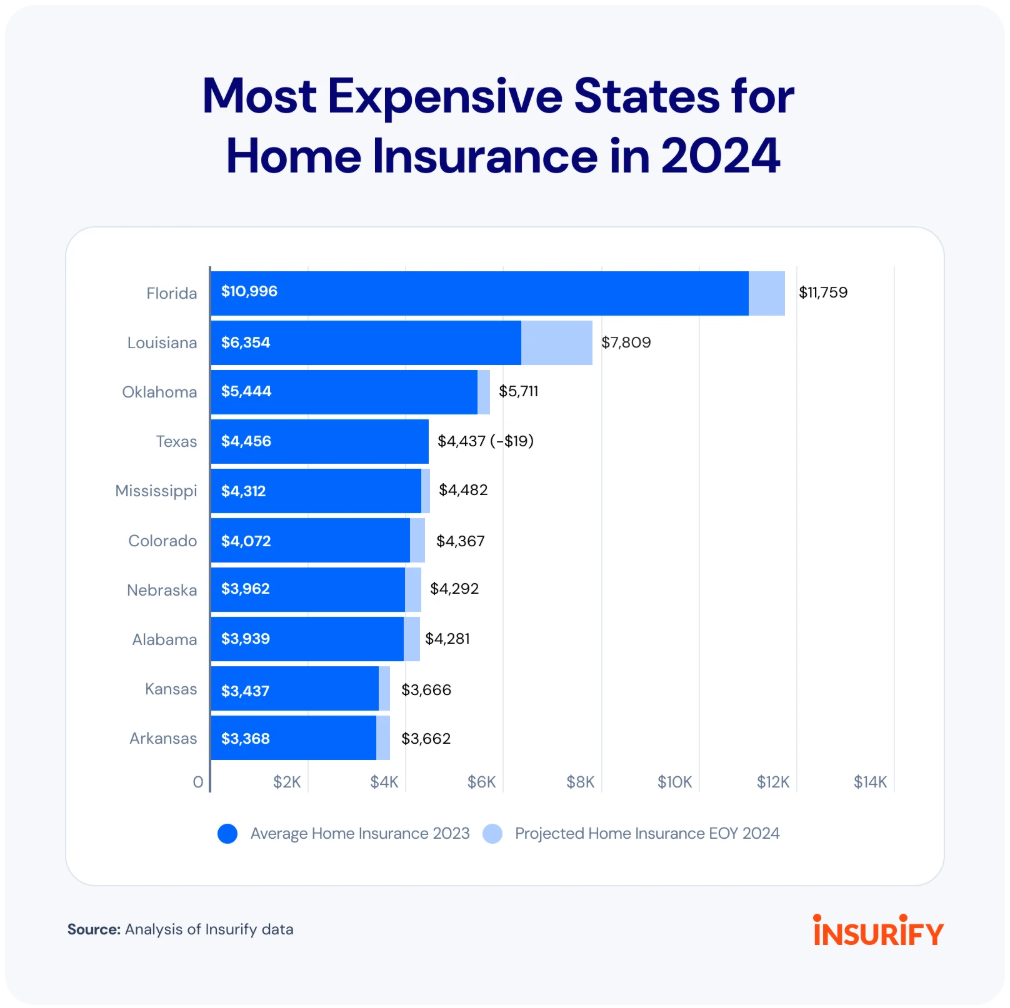

Both Florida and California have seen an exodus of insurers due to risk from severe storms (126 in Texas since 1980) and wildfires (7). Florida has become by far the most expensive state in which to purchase home insurance, but Texas is not far behind:4

As Insurers leave Texas, rules related to ESG criteria may protect policyholders or bear on the supervision of the financial health of insurers.

Given that insurers are already leaving Texas and that insurance premiums are already increasing, the Department of Insurance may need to intervene to ensure that policyholders are treated fairly and offered fair rates. State law dictates that insurance rates must be:

- Adequate

- Not excessive

- Based on sound actuarial principles

- Reasonably related to all costs

- Not based on an insurer’s race, creed, color, or national origin5

The American Academy of Actuaries has already recognized the “broad impact” of climate change on the actuarial profession. One result of this is of “historical data having decreasing credibility to inform actuarial assumptions in the short, medium, and long term.”6

This means, quite simply, that insurance rates that do not account for the risks of climate change are no longer based on sound actuarial principles and therefore do not comply with state law.

What can be done about this? We cannot stop severe weather, and we cannot stop insurers from leaving Texas. As the insurance market narrows, competition will decrease and rates will increase.

Consideration of climate risks will also make insurance rates increase. Faced with this reality, Texas has two choices: (1) refuse to accept the reality of climate change by banning rulemaking related to it (the SB 495 approach) or (2) impose some guardrails on insurers operating in the state.

ESG rules may be necessary to keep policyholders safe in Texas.

We encourage state lawmakers to take a forward-looking approach to this problem now. The Department of Insurance can establish regulatory guidelines on rate setting in light of climate risk factors. Insurers are going to account for climate risks either way—Texas can’t prevent that. Wouldn’t it be better for them to do so within a set of reasonable state regulations on the practice?

If insurance in coastal areas becomes more expensive, will insurers try to recoup those costs by raising rates in other parts of the state? One purpose of ESG policies, according to the NAIC, is to determine the financial health of insurers. Will Texas be able to do this if it is unable to make rules relating to ESG criteria and assessments? Shouldn’t our regulators have the ability to promulgate regulations relating to a common insurer practice?

In conclusion, we ask you not to vote SB 495 out of this committee. Texas is already dealing with the problem of insurance becoming more expensive due to climate change. Let’s give the Department of Insurance the tools it needs to address this problem.

WASHINGTON (Feb. 21, 2024)

NAIC Members Adopt Statement on ESG

The National Association of Insurance Commissioners (NAIC) has adopted the NAIC Statement on Environmental, Social, and Governance Policies for the insurance sector. Members unanimously adopted the following statement:

NAIC Statement on Environmental, Social, and Governance Policies

Environmental, Social, and Governance policies (ESG), however defined, have increasingly become a focus of discussion and debate among the financial sector, regulatory and legislative bodies, and other stakeholders domestically and internationally. In response to questions about the applicability of ESG policies to the U.S. insurance sector and its supervision, the National Association of Insurance Commissioners (NAIC), whose Membership is composed of the chief insurance regulators of all 50 states, the District of Columbia, and the five United States Territories, offers the following.

The NAIC does not anticipate developing regulatory policy to require or prohibit insurance companies from adopting ESG policies that govern insurers’ underwriting, investing, or other business decisions. However, we have extensive work underway on climate risk, race and insurance, corporate governance, and other related factors to the extent they directly pertain to our responsibility to protect policyholders and supervise the financial health of insurers.

The NAIC encourages insurers, regulatory bodies, standard setters, and policymakers to consider the reliability of metrics and the impact of ESG policies on the financial condition of insurers and the availability and affordability of insurance products and services, if adopting such policies.

The NAIC invites and encourages legislators, policymakers, and stakeholders to contact state insurance regulators when considering ESG-related legislation or executive action to discuss the potential impact of proposals on the solvency and financial stability of the insurance sector.

The NAIC is committed to providing an open forum for our Members and stakeholders to raise important issues, like ESG, that may impact our sector.

This statement on ESG evolved from discussions that state insurance commissioners initiated over the past few years, prompted by feedback and engagement from diverse stakeholders and the public.

About the National Association of Insurance Commissioners

As part of our state-based system of insurance regulation in the United States, the National Association of Insurance Commissioners (NAIC) provides expertise, data, and analysis for insurance commissioners to effectively regulate the industry and protect consumers. The U.S. standard-setting organization is governed by the chief insurance regulators from the 50 states, the District of Columbia and five U.S. territories. Through the NAIC, state insurance regulators establish standards and best practices, conduct peer reviews, and coordinate regulatory oversight. NAIC staff supports these efforts and represents the collective views of state regulators domestically and internationally.