Faces of Forced Arbitration

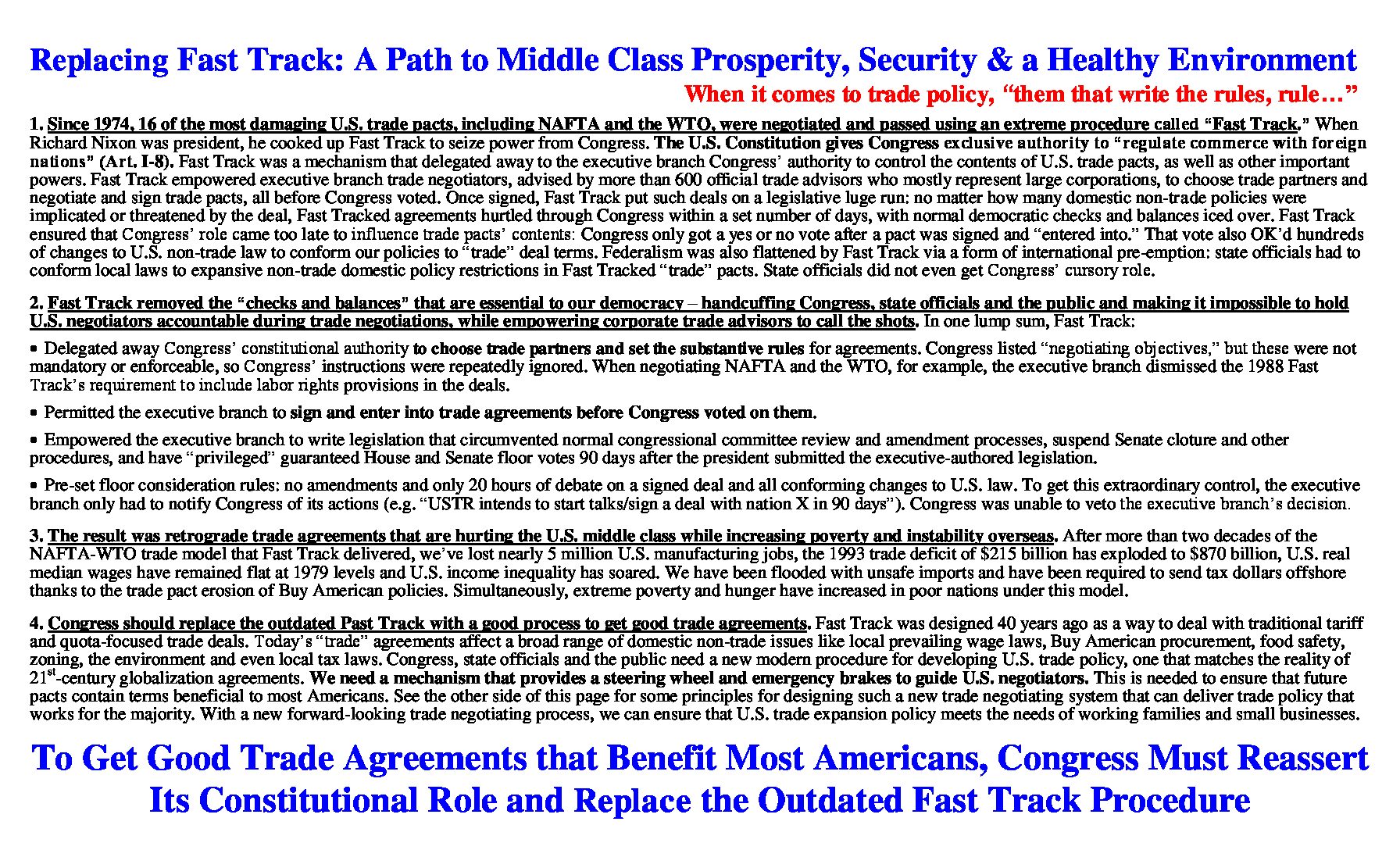

This afternoon, lawmakers introduced several pieces of legislation to curb the growing use of “ripoff clauses” and ensure harmed consumers, service members, students, and workers have a right to fight back in court against corporate wrongdoing. Known as forced arbitration, this practice strips Americans of any meaningful way to hold companies accountable for fraud or abuse and grants corporations a license to steal to pad its bottom line.

Forced arbitration no place in any system that is fair to everyday people. The bills introduced today would work hand-in-hand with a rule proposed by the Consumer Financial Protection Bureau (CFPB) to restrict the financial industry’s use of forced arbitration. Below are the stories of several real people harmed by forced arbitration, who would benefit from this newly-introduced legislation and the proposed CFPB rule.

Credit Cards

Tracy Kilgore, New Mexico

In July 2011, Tracy Kilgore went to a local Wells Fargo branch to change a signature card on behalf of the Daughters of the American Revolution, where she volunteered as Treasurer. Tracy did not personally bank with Wells Fargo or have any accounts with them. The bank teller asked her for her name and ID and began typing away her computer, and she promptly left once the change was processed.

Two weeks later, Tracy received a letter from Wells Fargo saying her credit card application had been rejected, though she never applied for one. When she saw the application was filed the day after she had visited the Wells Fargo branch, it became clear the bank tried to open a fraudulent credit card in her name. After Tracy found the rejected application was listed on her credit report, she called and wrote to Wells Fargo for months asking them to remove it. The bank kept saying it would take another 7-10 days, then another 2-3 weeks, to no avail. In the end, she never even got an apology.

Now, Tracy has joined with other defrauded customers in a class action lawsuit against the bank, but Wells Fargo is trying to force each consumer to fight them one-by-one in a biased and secretive arbitration system. Even though Tracy has never banked with Wells Fargo, their lawyers are trying to block her from suing them in court by pointing to an arbitration clause she never signed.

Auto Financing

Sergeant Charles Beard, California

Sergeant Charles Beard was about to be deployed to Iraq and asked for some help making his car payments. His lender, Santander Consumer USA, Inc., offered him a forbearance for a few months, but in exchange, had Sergeant Beard sign a modified lease agreement. Little did he know, a forced arbitration provision was buried in the fine print.

While serving his country in Iraq, Sergeant Beard fell behind in his payments. Men came to his home and repossessed the car – breaking federal law, which protects active duty soldiers by requiring lenders to obtain court orders before seizing their cars. Sergeant Beard brought a class action against the lender with other soldiers to enforce their protections under federal law, but their claims were thrown out due to a class action ban in the arbitration clause.

Payday Loans

Stephanie Banks, Oregon

In August 2013, Stephanie Banks made $15 an hour as a bookkeeper for the Salvation Army. To help pay rent for her and her son, she took out a $300 loan from the payday lender Rapid Cash, putting up the title to her car as collateral. Her interest rate was capped at 153.73% per year under state law. Soon after, Ms. Banks started chemotherapy to treat her lung cancer and retired from her job. A year later, she was in serious financial trouble, and had to declare bankruptcy. She listed the loan from Rapid Cash as a debt to discharge and finished the process in court with a lawyer.

Then, in August 2015, Ms. Banks almost had a heart attack when she received a letter from a collection service, claiming she owed Rapid Cash over $40,000. They threatened to destroy her credit if she did not pay immediately. Ms. Banks filed a free motion in court to dispute the $40,000 claim. Rapid Cash responded by pointing to an arbitration clause, buried in the fine print of the original agreement she signed two years earlier. The court ruled the clause still held and Ms. Banks would have to argue her case to a private arbitration firm chosen by Rapid Cash. To do this, she would have to pay $200 in arbitration fees, almost as much as her original loan.

Debt Relief

Bernardita Duran, New York

Bernardita Duran was 53 years old with only $700 in Social Security income when she paid an Arizona debt relief company to settle her credit card debts. Four thousand dollars later, Ms. Duran realized she had been scammed. She sued the company in New York federal court to get her money back, but the company pointed to a clause in their contract which stated her claims must be decided a private arbitrator – located in Arizona.

Ms. Duran protested that she could not afford to travel to Arizona, as it would cost more than a month’s worth of her income and prevent her from making rent. But the appeals court ruled that only the arbitrator in Arizona could decide if Ms. Duran could bring her claim in New York – meaning she would have to first travel across the country to Arizona to argue to the arbitrator that it’s unfair and unconscionable to force her to arbitrate her case there.

Private Student Loans

Matthew Kilgore, California

Ever since he was a child, Matthew Kilgore wanted to be a helicopter pilot. Mr. Kilgore thought he was on his way to achieving his dream when he enrolled at Silver State Helicopters, a for-profit aviation school that offered pilot training and certification. At the school’s recommendation, Mr. Kilgore took out a $55,000 private student loan from lender Keybank to cover his tuition. But Mr. Kilgore’s ambitions came to a sudden end in 2008 when his school abruptly went out of business and filed for bankruptcy, leaving students with tens of thousands of dollars in student loans but no marketable skills or diplomas. Since then, his loans nearly doubled to $103,000 with accrued interest.

Mr. Kilgore filed a lawsuit on behalf of himself and other Silver State students against Keybank to prevent them from enforcing their loan agreements or ruining the students’ credit. However, Keybank loan contracts contained an arbitration clause which prohibited class actions. An appeals court ruled the students would have to settle disputes with Keybank individually in arbitration. Meanwhile, other Silver State students who had similar loans with Student Loan Express, Inc. got $150 million in debt relief because their loan agreements did not include an arbitration clause.