The Numbers Don’t Lie: Obamacare’s Decline Is About Costs, Not Cheaters

By Peter Whoriskey

As millions of people were losing Affordable Care Act (ACA) coverage in 2026, Trump Administration officials said they were never eligible for it.

The people falling off the Obamacare rolls were cheating, according to the administration, and should never have been allowed to enroll because they misstated their income.

They’re wrong.

Enrollment in Obamacare is shrinking, falling from 22.3 million people in 2025 to an estimated 17.5 million in 2026.

“The only people who lost coverage were people who were never entitled to coverage,” Health and Human Services Secretary Robert F. Kennedy Jr. testified during an April 21 hearing before the House Energy & Commerce Committee.

Dr. Mehmet Oz, who oversees Obamacare as administrator of the Centers for Medicare and Medicaid Services (CMS), has gone further: He said current enrollment is “too high of a number” and he’d like to see millions more dropped from the program because so many were wrongly enrolled.

The Obamacare fraud claims are convenient for the Trump administration. As the midterm elections approach, they offer political cover for a significant problem of its own making: Millions of low- and middle-income Americans are losing health insurance this year because the administration pushed to cut the subsidies that made coverage affordable.

The administration’s explanation for declining Obamacare enrollment — that fraudsters are being purged from the rolls — has found its way into news coverage. But it doesn’t stand up to scrutiny. In fact, its core allegation is almost completely wrong.

This analysis by Public Citizen uses the government’s own statistics to debunk the administration’s claims.

The data indicate that the decline in Obamacare enrollment this year has nothing to do with removing deceitful enrollees. What the numbers show is that American families are being priced out of coverage.

The allegation of cheating embraced by the Trump administration predicts most of the fraud at a specific income level, right about the poverty line, where the incentives to misreport income are strong. If the administration’s fraud theory about the enrollment decline were true, a drop in the number of Obamacare enrollees at this income level would show up in the statistics.

But that’s not what is happening. The people losing coverage are concentrated at incomes well above the poverty line. They are low- and middle-income families whose premiums doubled after subsidies were cut. They didn’t cheat their way in. They simply can’t afford to stay in the program.

This year, after the subsidies were cut, Stacy Newton and her family — husband and two kids — of Wyoming, could no longer afford to pay Obamacare premiums, which amounted to $43,000 annually.

“The Trump administration keeps saying ‘it’s fraud, it’s fraud, it’s fraud,’” she said recently in an interview. “But I think they just want to break Obamacare and blame it on the people.”

GENESIS OF THE FRAUD THEORY

The fraud theory originated with the Paragon Health Institute, a nonprofit research organization closely aligned with the Trump administration and congressional Republicans. The group is led by Brian Blase, a former official in the first Trump administration. In January 2026, two Paragon directors joined the White House, and a senior policy analyst at Paragon became House Speaker Mike Johnson’s health advisor. The Paragon Health Institute has received money from the Koch Brothers’ Seminar Network and Leonard Leo’s The 85 Fund, both prominent funders of right-wing causes.

Launched in 2021, Paragon now stands as the most influential think tank for Trump healthcare policy. Under Oz, CMS has cited its findings to guide policy. Iowa Sen. Charles Grassley, chair of the Judiciary Committee, sent a letter to CMS citing Paragon’s fraud findings and demanding an explanation.

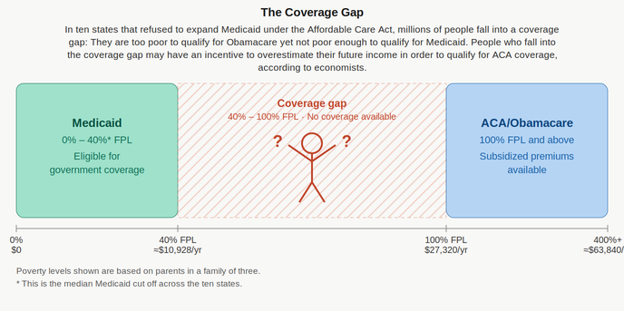

Paragon’s core claim rests on a quirk in the patchwork of American healthcare.[1] In the ten states that have declined to expand Medicaid, there is a coverage gap: millions of working-age adults do not qualify for Medicaid, often because their incomes are too high. At the same time, these working-age adults make too little money to qualify for Obamacare subsidies, which are available only to people with incomes above the poverty line. Paragon argues that millions of people in that gap are exaggerating their income — reporting just enough income to clear the poverty-line threshold and qualify for an ACA marketplace subsidy.

“There is a large incentive for people, particularly older people, to overestimate their income,” says Paragon in its 2024 report, The Great Obamacare Enrollment Fraud. “By misstating their income, these individuals get generous coverage at zero cost to them—instead of being ineligible for any subsidies at all.” (Older enrollees have more at stake, Paragon notes, because their premiums are higher.) In a 2025 follow up report, The Greater Obamacare Enrollment Fraud, Paragon says older people have a “massive incentive” to cheat this way.

The administration adopted this theory wholesale. In March 2026, CMS proposed a rule that scrutinizes income claims of this group, citing Paragon’s research.[2] In the administration’s version of events, this group of people — those falsely claiming income just above the poverty level — are dropping out of the program.

“The reduction in Obamacare enrollment,” Health and Human Services spokesman Andrew Nixon said in a statement earlier this year, “is largely due to CMS cracking down on fake and improper marketplace enrollments.”

The data, however, contradict Nixon’s claim. The fraud explanation fails in two key ways:

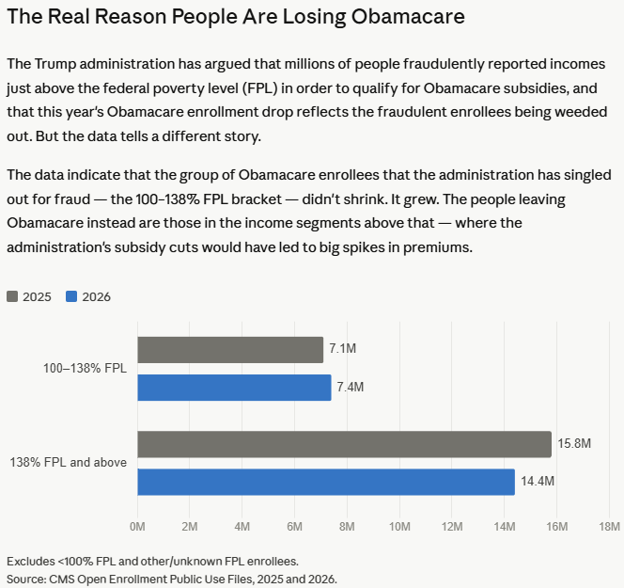

First, the drop in enrollment is happening in the wrong income group. If the administration’s theory were correct, the sharpest declines in enrollment would be seen just above the poverty line — exactly where Paragon says most of the fraudulent enrollees cluster. Instead, the opposite has happened: Enrollment in that income bracket has grown. The enrollment declines are concentrated at higher income levels. Almost half of the drop in enrollment comes among people with incomes more than four times the federal poverty level. These are not people gaming the poverty-line threshold. They are middle-income families who can no longer afford the premiums because they lost subsidies when the Republicans let them lapse.

Second, the drop is happening in the wrong states. Paragon’s fraud theory holds that 80% of the suspect enrollees — more than 5 million — were concentrated in the 10 states that did not expand Medicaid and so have a coverage gap. If the decline in ACA enrollment is to be explained by Paragon’s fraudulent enrollees dropping out, the ACA enrollment losses would be concentrated in those states. But that’s not what the data show.

As an example of one of those states, Paragon singled out Florida as a “clear outlier” where the fraud problem was “particularly acute,” estimating that more than 2.4 million enrollees were ineligible. Yet enrollment in Florida dropped by less than one-tenth that amount, and no faster than the rest of the country.

Numerous news accounts from across the country have documented that Americans are being priced out because the ACA subsidies were cut. These accounts are from North Carolina, Wyoming, Ohio and Tennessee. The preliminary Obamacare enrollment count showed only a 5% dip in preliminary figures released in March, but that number is expected to increase significantly as enrollees’ premiums come due. KFF projects that about 5 million Americans will lose Obamacare coverage in 2026.

WHERE THE TRUMP ADMINISTRATION’S FOCUS OUGHT TO BE

People living just below the poverty line in states that refused to expand Medicaid face a cruel trap built into the law: They have too little income to qualify for Obamacare subsidies, yet too much income to qualify for their state’s restricted Medicaid program. To escape the coverage gap, some have reported incomes just above the poverty line — enough to be eligible for the ACA marketplace.

The enrollment data bear this out. A peer-reviewed study in the American Journal of Health Economics found a suspicious clustering of reported incomes just above the ACA eligibility cutoff of $11,670 in 2015 — many enrollees reported exactly $11,670, $11,700, or $12,000 in income. “The enrollment data strongly suggest that some people in the coverage gap were able to obtain [Obamacare subsidies], perhaps by overreporting their income,” the authors concluded.

How many? Estimates vary enormously. A Congressional Budget Office letter last August, noting that such estimates are “difficult,” put it at 2.3 million for 2025. Paragon put the 2025 figure of ineligible enrollees at over 6 million, though that includes a broader range of alleged impropriety.

Paragon calls the overestimation of income fraud.[3] But consider who these people are. Their earnings fall below the poverty level; they’re guessing what they’ll earn next year and know that without insurance a health problem could be financially ruinous. Desperation and wishful thinking are not fraud.

The solution the Trump Administration proposes — removing these people from the ACA rolls — would not make them healthier or cheaper to care for. People in the coverage gap don’t disappear. They get sick and injured and they show up at emergency rooms. Federal law requires that hospitals treat them regardless of ability to pay. The burden of this uncompensated care gets shifted onto patients through higher prices, onto employers and people with private health insurance through higher premiums, and onto state and local governments through hospital subsidies. Refusing Medicaid expansion doesn’t eliminate the cost of caring for poor people — it just moves the costs off the federal ledger and onto everyone else’s.

References

[1] This quirk was created when the Supreme Court’s conservative majority ruled in the 2012 Supreme Court case NFIB v. Sebelius that states could decline the Obamacare Medicaid expansion.

[2] Under Oz, CMS has picked up on Paragon’s work and, in a rule last year, it singled out people in this income category for special scrutiny. Their applications are flagged if they projected income over the poverty line but other sources indicated they lived below poverty. The rule has been held up in the courts, but in Paragon’s version of events these are the bulk of the people who are ineligible.

[3] Paragon also has claimed as evidence of fraud that the large portion of Obamacare enrollees who never filed a claim is evidence of “phantom enrollees” who were signed up by brokers without their knowledge. That assertion has come under scrutiny by KFF here.